This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

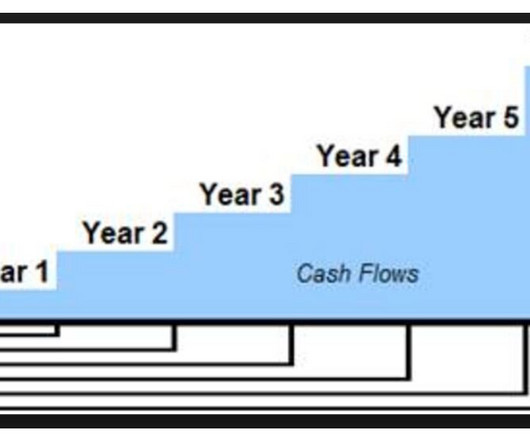

As I mentioned in my last post, DiscountedCashFlow (DCF) is a valuation method that uses free cashflow projections, a discount rate, and a growth rate to find the present value estimate of a potential investment. Per-share Equity Value = Equity Value / Number of shares outstanding.

To answer this question, three things are needed: The company’s intrinsic value: Typically based on cashflow streams available to shareholders, premiums paid in the marketplace, and scarcity associated with the target. The range of value: Typically depends on performance variables (sales, margins, and capital requirements).

Accurate and appropriate valuation is one of the pillars of maximizing the profits from a business sale. It’s integral to ensuring that the sale benefits all stakeholders and should be one of your priorities before advertising it to potential buyers.

per share significantly undervalued the stock of DFC. per share, 8.4% per share, by giving equal weight to: (1) the deal price, (2) a comparable companies analysis, and (3) a discountedcashflow analysis. per share, 8.4% Strine, Jr., DFC Global Corp. Muirfield Value Partners, L.P., 518, 2016 (Del.

It also provides tools to help sellers prepare their businesses for sale, such as financial analysis and market research. Additionally, Axial.com helps sellers find advisors and brokers to assist with the sale process. An advisor can provide invaluable guidance throughout the process, helping you to get the most out of your sale.

per share significantly undervalued the stock of DFC. per share, 8.4% per share, by giving equal weight to: (1) the deal price, (2) a comparable companies analysis, and (3) a discountedcashflow analysis. per share, 8.4% Strine, Jr., DFC Global Corp. Muirfield Value Partners, L.P., 518, 2016 (Del.

Watch E#84 Here Here is what my team and I learned from this interview: (These are notes from team members, writers, sometimes AI, and even listeners who submitted what i learned loosely edited and shared here) - If it seems a bit crude, you're reading our notes, so.

We see payables from customers, but not the long relationship and reputation that fostered those sales. sales or 7x EBITDA. Another potential problem is that the value, EBITDA and Sales figures reported may not be accurate for private companies. The DCF Approach has its own share of drawbacks as well however.

Here are the steps to define a company-specific M&A playbook: Establish clear objectives: Clearly define your company’s strategic goals, such as growth, expansion, diversification or increased market share, and how M&A can help achieve those goals. This will help you determine the appropriate value for potential targets.

Valuation methods can include discountedcashflow analysis, comparable company analysis, and precedent transaction analysis. The acquisition also provided Microsoft with access to LinkedIn’s vast user base and data, which it could leverage for its advertising and sales efforts.

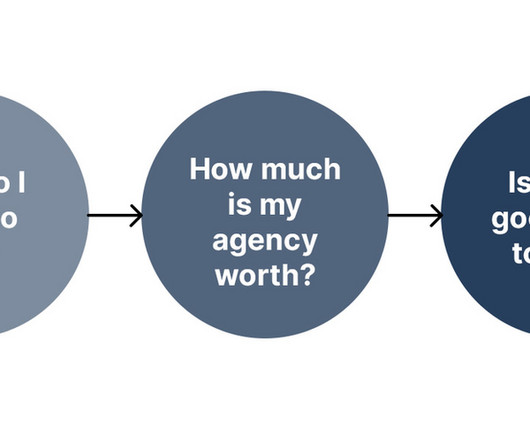

Other times, they are hoping to use their share of the sale to alleviate personal debt. The table below outlines a few key criteria that you should consider before going through with a sale: Should I Sell My Insurance Agency? Are looking for a career change. Personal Considerations How Much Is My Agency Worth?

Gregory's vast experience is laid bare as he shares the differences in valuation methodologies, adapting from roles in home building business operations to being a leading business valuator. His insights into the industry's standards offer a unique perspective, particularly with the challenges surrounding price versus value concepts.

Asking the right questions upfront can reveal whether a broker is the right strategic partner for your business sale. If you own a manufacturing firm, collaborating with a manufacturing business broker who knows production processes, supply chains, and industry benchmarks could significantly speed up your sales.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content