This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thus far, we have discussed many aspects around capital structure and debt financing, including how debt levels are determined by a company’s cash flows, enterprise value, and asset values. This post is the last one of our debt discussion. ABL can exists alongside other types of debt (revolver, term loan, etc.)

Ask anyone interested in distressed debt hedge funds for “the pitch,” and they’ll probably mention one of the following: “It’s like long/short equity or credit , but more interesting!” These are nice sales pitches, but the reality is quite different. Distressed investing offers equity-like returns with lower risk.”

“Event-driven hedge funds” is one of the more confusing labels in finance. Part of the issue is that many different strategies fall within the “event-driven” category: merger arbitrage , activist investing , distressed investing, special situations, and more. By contrast, an event-driven fund would never bet on such a situation.

Balancing debt and equity components are crucial to minimizing the cost of capital while maintaining financial flexibility. In general, this focus on cash flow will enable timely debt servicing and can allow the acquired company to bounce back stronger than ever before being taken public or spun off to another private equity firm.

In the event of a sale, would it be you who is receiving liquidity—or are you the one providing it? The younger partners were presented with a dilemma: They could each increase their stakes in the business and collectively control it but would have to take on—and be personally liable for—the $25 million in debt.

Capital is generally grouped into three main classifications: Senior Debt, Mezzanine Capital and Equity Capital. Most entrepreneurs are very familiar with senior debt offered by traditional banks. Senior debt is first in seniority and is often secured by collateral in the form of a lien.

” Thus, the MAE qualification renders some adverse events irrelevant and non-actionable under the agreement. In both contexts, however, the seller will want to minimize the likelihood of occurrence of an MAE by narrowing which events and circumstances will satisfy the definition, and the buyer will seek to achieve the opposite.

The decisions from the court on those preliminary matters, as well as the arguments raised by legal counsel, offer some valuable lessons for sellers considering sale transactions that require debt financing, and may motivate sellers to re-evaluate certain provisions and remedies that have become customary in those transactions.

The sale proceeds that the seller contributes to the transaction, which is commonly referred to as rollover equity , provides an opportunity at a “second bite of the apple” when the PEG later sells the company in a 3–5-year time horizon. US PEGs still have approximately $1.1

McCormick of the Delaware Court of Chancery granted sellers specific performance in a breach of contract action against buyers KCAKE and Kohlberg Funds, arising out of the sale of DecoPac Holdings Inc. ("DecoPac"). Snow Phipps Group, LLC., KCake Acquisition, Inc., 2020-0282-KSJM (Del.

Overall, banking increased 17% – largely driven by this impressive performance in investment banking as well as “bolstered by a rebound in debt issuance and some signs of life in the equity capital markets”. Throughout Q3 Citi has had some significant changes to its personnel.

If you have been through a business purchase or sale, you have likely experienced the unique tension and strife common to that phase of the deal known as “due diligence.” While it takes work, due diligence helps squeeze risk out of a sale, protecting the buyer and the seller. The benefits to the seller may not end there, Frye noted.

Founder Tips for Selling Your SaaS Company Within One Year By now, you have improved all the metrics, tech-debt, and related things that you can do (won’t be everything)! Before preparing your company for a potential sale , you must be emotionally, strategically, tactically, and physically ready. Timing is also essential.

McCormick of the Delaware Court of Chancery granted sellers specific performance in a breach of contract action against buyers KCAKE and Kohlberg Funds, arising out of the sale of DecoPac Holdings Inc. ("DecoPac"). Snow Phipps Group, LLC., KCake Acquisition, Inc., 2020-0282-KSJM (Del.

the order in which investors get paid in the event of a sale or liquidation) Anti-dilution provisions to protect the investors' equity stake The terms for conversion of preferred stock into common stock Any management or governance changes required by the VC firm 2.

The recent purchase of Riverbed Technology LLC reflects a burgeoning niche for middle-market technology turnaround investor Vector Capital Management LP: buying companies from lenders who converted debt to equity through reorganizations. reported that Riverbed’s sales came to about $535 million for the 12 months ended Sept.

In the podcast, Kirk Michie mentions that his primary goal is to help clients get to the right investment banker and M&A attorney, as well as prepare them for maximizing their deal's potential sales price and protecting against potential pitfalls. The speakers also touch upon the perspective of the buyer in a sale transaction.

A classic example of T-Bills in action occurred during the European Sovereign Debt Crisis. Investors, wary of the uncertainties in European debt markets, turned to U.S. Debt Ceiling Crisis , T-Bills experienced an unusual yield spike as investors momentarily questioned U.S. Represented by the full faith and credit of the U.S.

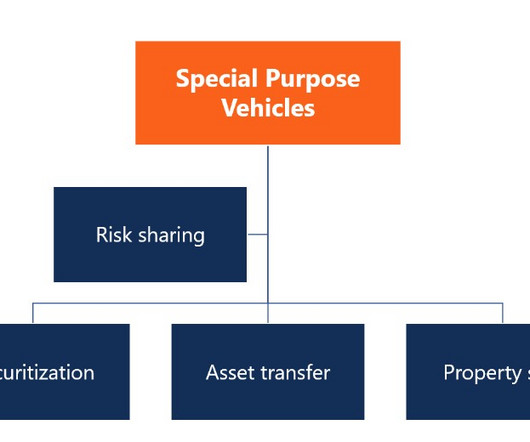

The proceeds from these sales are then used by Company B to issue securities that are sold to investors. In the event of the parent company's bankruptcy, the SPV remains solvent, and its obligations are not affected. For instance, a company laden with debt could transfer some of it to an SPV, thereby reducing its debt-to-equity ratio.

In reaching this order, the court applied the prevention doctrine, finding that the unavailability of buyer’s debt financing did not permit buyer to circumvent its obligation to close because buyer materially contributed to the debt financing being unavailable. All of those demands were rejected by the lenders.

Recapitalization is a process of restructuring a company’s debt and equity mix, also known as its capital structure. Selling a portion of the business also means giving up some control and share in future liquidity events, however. In the software industry, debt recapitalization can be a particularly useful tool.

But the events of 2023, including the UBS acquisition of Credit Suisse and the rise of firms like Wells Fargo, Jefferies, and RBC, have shaken up the traditional list. The name “bulge bracket” (BB) comes from the prospectus for an IPO or debt issuance, which lists all the banks underwriting the deal.

Remember that, normally, a bank issues loans and then finds the liabilities (deposits, debt, etc.) Immediately after this sale, the bank also announced plans to raise additional equity and convertible preferred stock. to back them. But commercial banking is a different story.

The offer of ongoing ownership is known as “rollover equity” because the seller chooses to roll a portion of the sale proceeds back into the company’s new ownership structure. You would make $95M after paying off the company’s debt and transaction expenses. What is Rollover Equity? Ongoing financial benefits.

From assessing its value to transitioning ownership, understanding the nuances of your industry is crucial for a successful sale. Assessing the Value of Your Small Business The accuracy of your business’s valuation is essential for a successful sale. Here’s a comprehensive guide to help you navigate selling your business.

Deals with debt multiples higher than 6X EBITDA rose to greater than 75% of the total, again the highest in history, and in dramatic contrast to the years following the 2008 financial crisis, when the number gradually increased from nearly zero to about 60% by 2017. Over 70 PE firms involved themselves in our sales processes.

One of the roadblocks that commonly arise in structuring a business sale stems from differing viewpoints of value. If the sale occurs in a high-interest-rate environment, an earnout can help narrow the gap created by debt coverage. Most sellers see maximum profit potential, while most buyers see risk and past earnings.

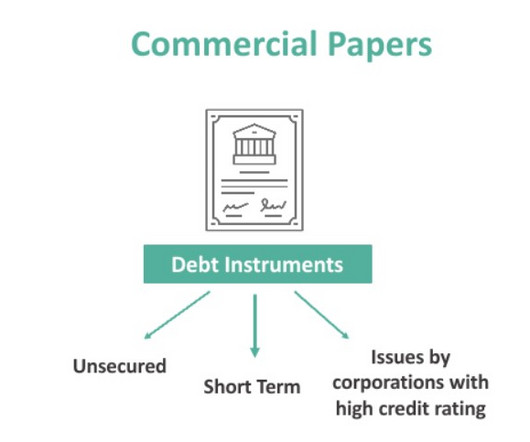

Commercial paper is a form of unsecured short-term debt. Because of its short duration, commercial paper allows issuers to manage immediate liquidity needs without locking into long-term debt. For instance, a company might issue commercial paper to finance inventory ahead of a peak selling season, repaying it once sales are realized.

Additionally, at the exit of the investment period, the value of retained ownership increases with debt repayments and equity appreciation resulting from both organic and inorganic growth, making liquidity generated at exit typically more meaningful than the initial sale – an event often referred to as “the second bite of the apple.”

Debt and liabilities: assess the company’s debt levels and liabilities to determine whether it can manage its obligations during economic uncertainty. What is the target company’s current debt position, and what is their plan for managing any potential financial risks that may arise due to the economic uncertainty?

While overall M&A activity among tire retailers, wholesalers and commercial tire dealerships remains active but noticeably slower, it’s harder for wholesalers and commercial tire dealerships to have a saleevent as compared with retailers. The debt in an ESOP is very, very difficult to restructure,” says Beard. “In

Michael and his wife have achieved success without taking on any investors or business agents, and without any debt in their balance sheets. The team has also professionalized the sites they acquire by using better SEO tactics, better content strategies, and optimizing the sales processes. billion monthly users.

minutiae about issues like OID for debt issuances ) and did not accurately represent a 1- or 2-hour case study. Procyon is spending aggressively on sales & marketing, resulting in negative Net Income, a declining Shareholders’ Equity, and a negative Cash position. They over-complicated the financial model (e.g.,

For example, a highly aggressive monetary policy, external shocks, and substantial debt. On account of implementation, response, and recognition lags with regard to macroeconomic policy , such events can lead to a recession so quickly that policymakers would not be able to set up an effective defense.

Professional networks and industry events: Leverage your professional networks and attend industry events to gather insights and identify potential targets. Identify integration workstreams : Break down the integration process into distinct workstreams, such as finance, operations, HR, IT, and sales and marketing.

If you Google this topic and look at the results, you’ll find articles and discussions about LBO models and points like the returns attribution analysis : This type of “value creation” measures the returns sources in a buyout deal: Debt paydown vs. multiple expansion vs. EBITDA growth. Why is PE Value Creation Suddenly “Hot”?

Last week in our first installment titled “ Separation for Success – Divesting for Maximum Value ,” we covered how to master the divestiture process by upgrading your pre-sale planning approach and the importance of playing both “offense and defense” in when preparing a business to be divested. Determine the Day-1 operating model.

Founder Tips for Selling Your SaaS Company Within One Year By now, you have improved all the metrics, tech-debt, and related things that you can do (won’t be everything)! Before preparing your company for a potential sale , you must be emotionally, strategically, tactically, and physically ready. Timing is also essential.

A private sale can be structured to achieve a complete exit for existing equity holders, with possible deferred consideration, earn-outs and escrows. Stock market forces also make the timing of an eventual outright exit and the final blended valuation of equity sales over time uncertain.

In regions like London and Hong Kong , ACs are used for investment banking , sales & trading , and other areas at banks and consulting firms. Social/Networking: Finally, there may be a networking panel or “social event,” such as a group lunch, which will take another 30 – 60 minutes. How much would it be worth? Why or why not?

Finance and Banking Debt Collection IVR systems can be used to automate debt collection processes, sending reminders and facilitating payment arrangements. Event Management Ticket Sales IVR can be used to sell tickets for events, providing a convenient and accessible option for customers.

A word of caution, though: In many circumstances (including the sale of a company), management’s standalone long-term forecasts may be strategically provided to counterparties, utilized by the board’s financial advisers in their fairness analysis and publicly disclosed in filings with securities regulators.

The Shadowy and Elusive Series of Events. The lawsuit arose from the contemplated sale of a hotel portfolio, consisting of 15 luxury hotels located throughout the US. billion, a portion of which was to be funded with third-party debt. Key Takeaways. Seek Permission Rather than Forgiveness.

As Jean-Charles Sambor, head of emerging market debt at TT International Investment Management tells The TRADE: “The emerging markets fixed income sphere is recovering, and we expect inflows back to the asset class after years of investor exodus.” But, of course, there is more to come, and the market is prepping.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content