This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Understanding the role of carried interest in private equity, real estate, and hedge funds. Carried interest (or carry) is a way of rewarding professional investment managers with a share of an investments anticipated profits.

As I mentioned in my last post, Discounted Cash Flow (DCF) is a valuation method that uses free cash flow projections, a discount rate, and a growth rate to find the present value estimate of a potential investment. The major steps of DCF are: Identify extraordinary, unusual, non-recurring items from the target’s 10-Ks and 10-Qs.

Calculating cost of debt, cost of equity, and weighted average cost of capital (WACC). Determining the year-by-year future non-equity claims from the latest 10-K, especially those that will occur during the forecast horizon, and their combined present value. Tangible Book Value = Book Value of Equity - Goodwill.

Over the past few decades, growth equity (GE) has gone from an afterthought to a major asset class for huge investment firms. Some argue that GE offers the best of both worlds: the opportunity to fund innovation and growth – as in venture capital – plus the ability to limit downside risk and invest in proven companies – as in private equity.

Because dividends is a piece of equity, we can use the Capital Asset Pricing Model (CAPM) to calculate the proper Rate of Return (r). To perform this forecast, we need the target’s dividend history again, the book value of equity and year-end shares outstanding, and the stock prices at year-end.

Equity Value (today) = Equity Value at end of forecast period/ (1+Target rate of Return)^n 4) Because this is the valuation of the start-up before the VC invests his/her money in the business it is known as Pre-Money Valuation of the start-up 5) VC investors receive an equityshare of the business in exchange for their investments.

Discounted Cash Flow (DCF) i s a valuation method that uses free cash flow projections, a discount rate, and a growth rate to find the present value estimate of a potential investment. Information listed in the DCF analysis: See the items listed under DCF above. A 5- or 10- year historical data is preferable.

If you’ve ever thought that Buyside might be for you — whether it be Growth Equity, Private Equity, Hedge Funds, Corporate Development, Venture Capital, etc. A Few Reads to Digest Valuation Simplified: How Discounted Cash Flow Modeling Drives Financial Analysis Harness Discounted Cash Flow (DCF) modeling for financial analysis.

It is calculated by multiplying the current share price by the total outstanding shares. This metric provides a quick snapshot of a company’s total equity value as perceived by the stock market. DCF is particularly useful for valuing startups or companies with predictable cash flow patterns. million + $1.65

Watch E#84 Here Here is what my team and I learned from this interview: (These are notes from team members, writers, sometimes AI, and even listeners who submitted what i learned loosely edited and shared here) - If it seems a bit crude, you're reading our notes, so.

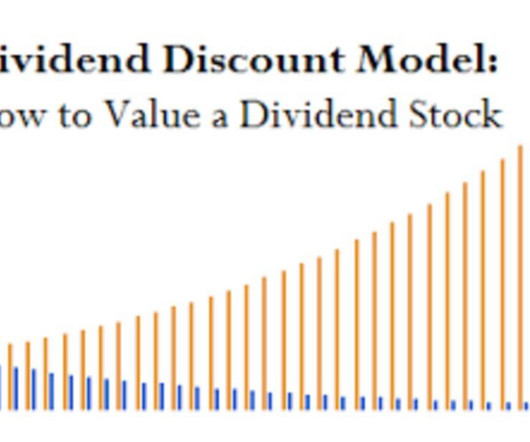

It can be useful for certain companies, such as power and utility firms and midstream (pipeline) operators in oil & gas … …but it’s also much harder to set up and use than a standard DCF. And Equity Real Estate Investment Trusts (REITs) must distribute almost all their Net Income, so the DDM can work well in REIT valuations.

. ("Dell") by its CEO and founder, Michael Dell, and affiliates of a private equity firm, Silver Lake Partners ("Silver Lake"), at $13.75 per share significantly undervalued the stock of Dell. per share reflecting an approximate 28% premium. per share reflecting an approximate 28% premium. 565, 2016 (Del.

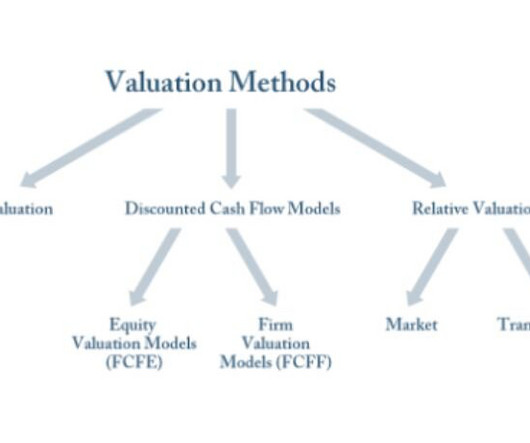

Thus far, we have discussed five valuation methods: DCF, Comparable Company, Precedent Transaction, LBO, and Dividend Discount Model (DDM). For the purpose of our post, the output variables should be the per-shareequity value returned from our DCF, Comparable Company, etc. valuation exercises. is returned in 6.7%

. ("Dell") by its CEO and founder, Michael Dell, and affiliates of a private equity firm, Silver Lake Partners ("Silver Lake"), at $13.75 per share significantly undervalued the stock of Dell. per share reflecting an approximate 28% premium. per share reflecting an approximate 28% premium. 565, 2016 (Del.

But in capital markets, you work on just one category of deals , such as equity-related transactions (IPOs, follow-ons, convertible bonds, etc.) so you may look up stats on recent issuances and share them with the lead team – but you are not heavily involved in the process. Why not accept a capital markets role?”

share, which represented the portion of the deal price attributable to projected synergies. share to reflect the change in value of the target between signing and closing. share, a 2.67% increase over the deal price. share for changes in Regal’s value between signing and closing, which was less than the $7.32/share

As opposed to merely focusing on the market capitalization, which only accounts for the company’s equity value, the Enterprise Value Calculator considers the company’s debt, cash, and other financial liabilities. Discount Rates Discount rates are used in the DCF method to determine the present value of future cash flows.

Q: Why not private equity, growth equity, hedge funds, or entrepreneurship? Growth equity is a bit closer, but you’re more interested in early-stage companies that need VC support rather than already successful companies that need more capital. Q: What’s the difference between pre-money and post-money valuations?

Metals & Mining Investment Banking Definition: In metals & mining investment banking, professionals advise companies that find, produce, and distribute base metals, bulk commodities, and precious metals on debt and equity issuances and mergers and acquisitions. What Do You Do as an Analyst or Associate in the Group?

This site has already covered investment banking interview questions , private equity interview questions , and venture capital interview questions , so the next topic on the list seemed to be growth equity interview questions. Q: Why growth equity? Q: Walk me through your resume.

Its more of an industry focus at the intersection of several other strategies , such as long/short equity , event-driven investing , and even merger arbitrage. While plenty of bankers and equity research professionals from healthcare teams enter biotech hedge funds, people with advanced degrees (M.D.,

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content