This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The stock opened that day at $69.69, or 34% above its IPO, and closed up nearly 29% at $67 per share. The overwhelming positive sentiment from Wall Street has rewarded the company's decision to go public after a lengthy dry spell for IPOs. Here's what analysts at some of the biggest shops on Wall Street had to say on the IPO.

Founded in 2019, Okay participated in Y Combinator’s Winter 2020 cohort before going on to raise a total of $6.6 They were u sually companies in the pre-IPO phase with hundreds to thousands of engineers where the manager wanted to start tracking what others are doing, and looking for tools to help with decision-making.”

In that environment, very few firms sought IPOs, and there was a major slowdown in overall exits, whether private or public. And will that mean that some of the privately held management consulting firms or other professional services companies will choose an IPO this year? But those companies have been public for more than 20 years.

Before joining HKEX, she was a partner of Davis Polk & Wardwell from 2010 to 2019, where she oversaw a wide portfolio of clients in Hong Kong and across Asia. Prior to that, she served as the head of IPO transactions, listing division, HKEX from 2007 to 2010. “It

It is a reasonable extrapolation – and we are nothing at Cooley if not wildly reasonable – that more operating companies are considering going public through a merger with a SPAC (commonly referred to as a backdoor IPO) since the beginning of time. Read full article. Contributors. Dave Peinsipp. Charlie Kim. John McKenna. Yvan-Claude Pierre.

since its IPO in April 2019 until the end of 2019. The data supports this theory, as during the period from March 13, 2020 (when the US declared Covid-19 a national emergency) until August 21, 2020, Zoom had a negative beta of -0.39. This was a dramatic change from its pre-pandemic days when it had a positive beta of 1.81

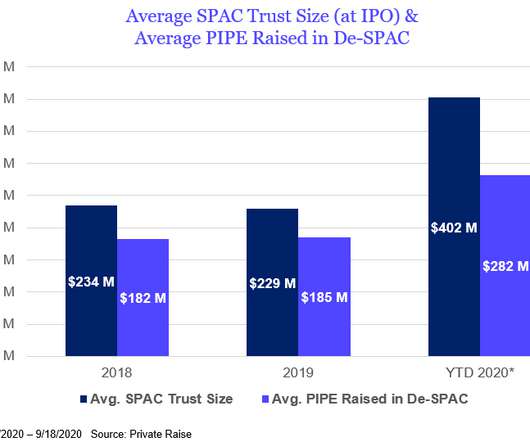

is the increased frequency at which SPAC IPOs are occurring. As reflected in Chart 1 , 102 SPAC IPOs have been announced this year as of September 18, 2020—almost double the number of SPAC IPOs in all of last year (and more than double the number of SPAC IPOs in 2018). SPAC vs. IPO. A distinct feature of SPAC 3.0

YoY decline in the total monetary value of VC investments compared to Q2 2019 and an 18.0% YoY in total value compared to 2019 and down only 11.3% Second, the IPO market, a key exit avenue for VC investments, proved increasingly strong and resilient throughout the year. These were just a few of many strong IPOs seen this year.

Following the completed merger, Redburn Atlantic will now operate as the equity capital markets execution arm of Rothschild & Co, with the aim of delivering participations for clients in IPOs, placements and block trades.

According to Nasdaq , in 2015, SPACs made up approximately 12% of the IPO market, but by 2020, that number had risen to approximately 53%. SPACs are predicted to be an even higher percentage of the 2021 market share, with SPACs representing 79% of the January IPOs. In In re Benjamin H.

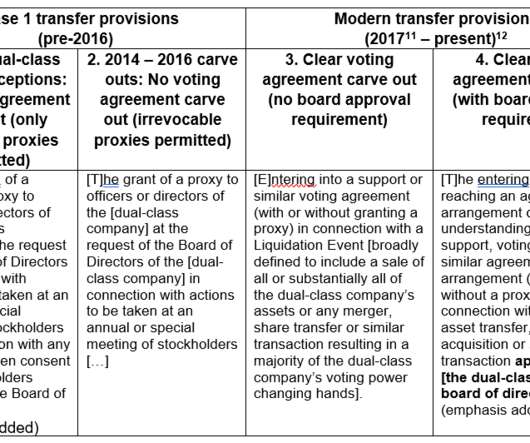

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders. Potential carve outs for M&A voting agreements. Stockholder litigation.

government shutdown disrupting the market for IPOs, Brexit uncertainty, natural disasters and various other crises, cross-border M&A activity momentum continues. The following 10 key trends are underpinning hyperactivity in global M&A markets and are set to continue to shape deals well into 2019. Finally, with the U.K.

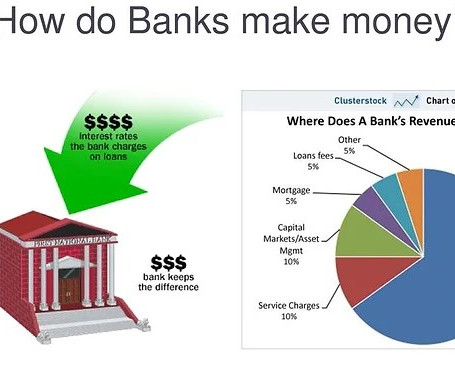

These charges were in the spotlight in 2019 when U.S. 2019 was a notable year for trading, especially for banks like J.P. When Facebook went public in 2012, it needed an investment bank to handle the Initial Public Offering (IPO). Some banks charge both the sender and receiver. banks accumulated over $11 billion from them alone.

M&A is a central part of SymphonyAI’s growth strategy as the company prepares for a potential private placement and, eventually, an IPO. “We’re He led the Cerence’s 2019 spinout from conversational AI tech developer Nuance Communications Inc. Dhawan previously ran Cerence Inc. which Microsoft Corp.

For example, in the 2012 Facebook IPO, common shareholders gained exposure to the tech giant's fortunes, while also securing a say in corporate matters. CEOs, declared in 2019 their commitment to lead their companies for the benefit of all stakeholders, marking a significant shift from previous shareholder-first dogmas.

Other recommendations from Kent include allowing greater access to investment research for retail investors, involving academic institutions in supporting investment research initiatives and reviewing the rules relating to investment research in the context of IPOs.

As SPAC IPOs broke records – in both value and volume – in 2020 (and again in 2021), it was inevitable that stockholder litigation would follow. Churchill was incorporated in Delaware in October 2019 and closed its $1.1 billion IPO in February 2020. On January 3, in In re MultiPlan Corp. Stockholders Litigation (Del.

Strained access to public markets and funding The IPO market remained relatively inactive in 2023, leading many life sciences companies looking to raise funds to turn to other exit strategies. Additional major acquisitions of 2023 included Pfizer’s acquisition of Seagen for $43 billion and Merck’s acquisition of Prometheus for $10.8

of investments each year: Typically 8-10 companies per year (based on 2019 and year to date 2020) Previous companies invested in: 165, including ContactEngine, Improbable and Sprout.ai. of investments each year: 12 Previous companies invested in: 216, including Bnext, GoStudent, Housfy and ShipHawk No.

Although global deal value was a subdued $966 billion in the first half of 2020 (down nearly 50% compared to the first half of 2019), momentum skyrocketed in the second half of the year to nearly $2.2 compared to 2019. compared to 2019, and up even higher (57%) when looking solely at US deal value. COVID-19: The New Normal.

The MLB started allowing PE ownership in 2019, and the NHL followed suit in 2021. Exits seem dependent on finding another PE firm or consortium willing to pay more, and options like IPOs and acquisitions by “strategics” (normal companies) are less viable due to league rules on ownership.

If 2019 was the year of life sciences mega-deals, 2020 was the year of COVID-19, as the global pandemic permeated every aspect of the dealmaking landscape, with the life sciences sector being no exception. billion deal inked in 2019 that included more than $2 billion in contingent payments based on the achievement of certain milestones.

on transactions over 2019’s mega?mergers. A healthy 90 biopharma M&A transactions were announced in 2021 (compared to 69 in 2020 and 70 in 2019, the most transactions since 2016). But deal value – which totaled $108 billion as of December 15, 2021 – was slightly down from 2020 and significantly down from 2019.

Apptio itself has grown over the last several years with its own acquisitions, specifically buying Cloudability in 2019 , TargetProcess in 2021 and Cloudwiry in 2022. The second is that it’s worth watching to see what happens next across the PE landscape.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content