This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

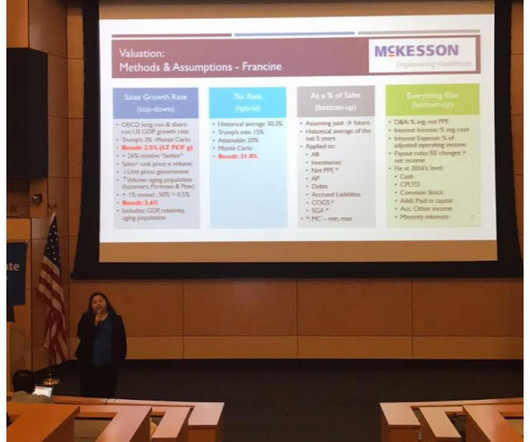

On this very last valuation blog post, I'd like to walk us through a presentation I made back in April 2017 as a part of my master in finance fellowship Capstone presentation.

As I mentioned in my last post, Discounted Cash Flow (DCF) is a valuation method that uses free cash flow projections, a discount rate, and a growth rate to find the present value estimate of a potential investment. Calculate the Equity Value and the per-share Equity Value - this number would serve as the base case share price valuation.

Peaked market valuations: When market cycle peaks or an industry fully matures, it may be advantageous for shareholders to cash out. Buying and selling a company has many overlaps to buying and selling a house. the house failed to increase in expected value), mature market (i.e. inheritance), and conflict among owners (i.e. divorce, etc.).

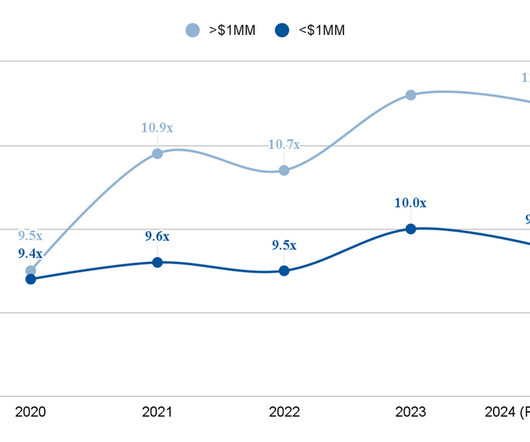

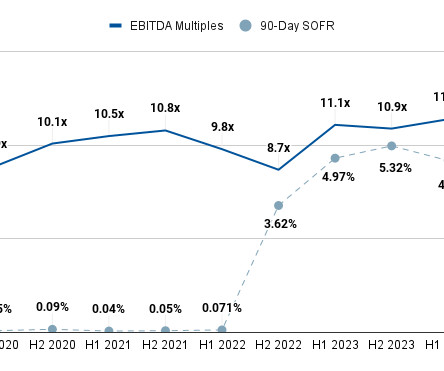

The following report contains our projections for Q3 2024 insurance broker valuation multiples. Insurance Broker Valuation Multiples: Q3 2024 Projections Using these numbers as a baseline, let’s examine the insurance industry more closely to identify influential factors behind its specific changes.

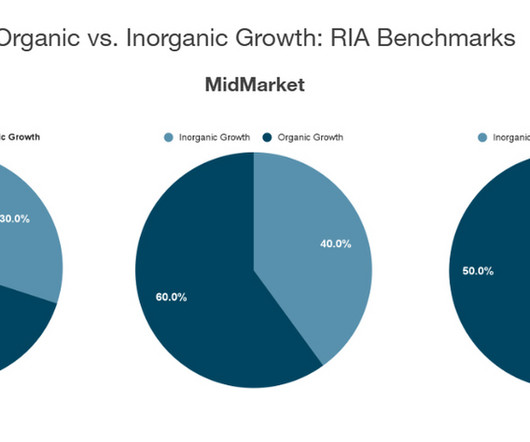

The following article examines valuation multiples for registered investment advisor (RIA) firms as of 2024, based on data gathered from our SF Index and available third-party sources. By Fee The following table outlines just a few key takeaways about various fee structures commonly found in RIAs as they apply to M&A transactions.

As one of the most active M&A firms in the insurance sector, we are frequently asked how insurance agency valuations work. This article discusses the fundamentals of insurance agency valuations, plus a few lesser-known factors that play into these processes before we give an overview of the insurance M&A market in 2024.

The following report examines the health and outlook for insurance M&A deals in 2024. We base this research on several key findings in our proprietary SF database, which observes and records data from the top ~400 insurance M&A buyers. Company: Which Is The Better Insurance M&A Deal?

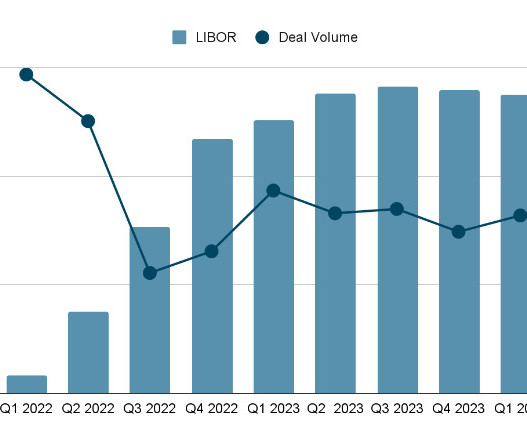

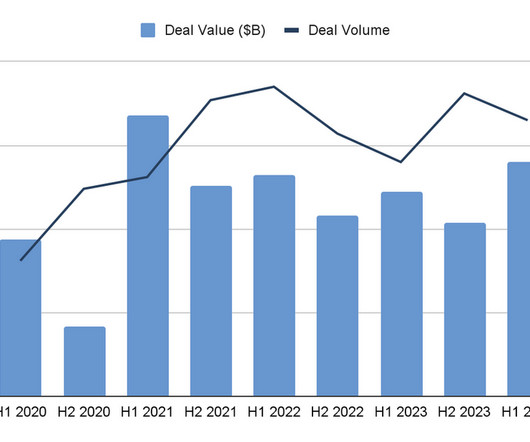

M&A transactions for insurance companies are part of a robust but complicated market that requires ingesting a great deal of data in order to fully understand. While insurance M&A did see slight dips in deal volume and average value (Fig.2)

The insurance M&A market in 2024 is significantly more complex now than it was 20 years ago. However, this report seeks to make sense of these qualities as a whole to provide an overview of the 2024 insurance M&A market. The table of contents below offers quick links for readers seeking specific information in later sections.

We strongly recommend that you speak with a reputable M&A advisor before running an M&A deal process. Insurance agency valuation is a critical component of running an M&A deal, but executing this multi-step process well requires a great deal of specialized education and experience.

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

In it, we provide readers with a quick and simple overview of the current insurance brokerage M&A market , after which we discuss several macroeconomic and industry-specific factors that could drastically affect transactions in the next six months. The market is already highly competitive, but it’s also limited to what buyers can afford.

The following report details insurance brokerage M&A multiple averages for H1 2024. Insurance Brokerage M&A Multiples: Market Overview The 2020s have proven to be a complex market for insurance brokerages. Because several kinds of insurance are legally required (e.g., Streamlined Operations.

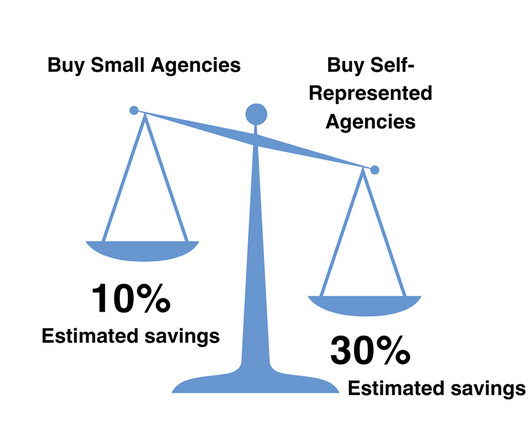

On average, company leaders in any industry who attempt an M&A transaction using an in-house team average 30% less once the deal is complete. Below, we offer a basic breakdown of the most common advisors in an M&A transaction. The two most common types of M&A buyers are: Strategic. Retirement. Financial Security.

What’s on tap for 2018 M&A? A recap of 2017 trends and the Cooley outlook on this year’s dealmaking: Buying Innovation: Retention and Non-Competes. As an example, for California specific requirements, see our prior blog post Non-Competes for California Employees in M&A Deals: Don’t Fudge It.

Compensation matters, including retention packages, equity treatment and related disclosure, are always key negotiating points in M&A transactions. In this post, we discuss compensation challenges in M&A deals in a depressed market and how dealmakers can address these issues.

S&P Global’s 2023 Market Intelligence League Table Released NEW YORK, NY - February 8, 2024 - Sica | Fletcher, a premier financial advisory firm, retains its commanding presence in the #1 spot on S&P Global’s Market Intelligence League Table, a position the firm has held quarter-over-quarter since 2017. Learn more at SicaFletcher.com.

Who Performs A Valuation? RIA valuations are typically performed by one of three parties: The M&A Advisor A Third-Party Specialist The Seller Themselves Although many sellers attempt to perform their own valuations, we strongly recommend against this.

M&A is a central part of SymphonyAI’s growth strategy as the company prepares for a potential private placement and, eventually, an IPO. “We’re Founded in 2017, the Palo Alto, Calif., billion valuation in 2021. The post On the Hunt: SymphonyAI’s M&A Algo appeared first on The Deal.

Insurance agency owners who are considering the prospect of running an M&A deal process often have many concerns about the fate of their agencies, but the most common by far are those surrounding the agency’s purchase price at closing. The following section describes this process in further detail.

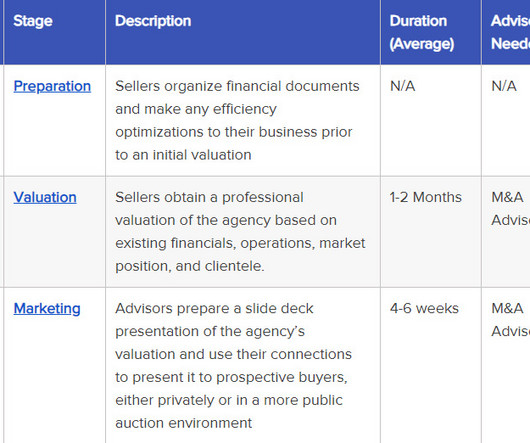

This article presents a step-by-step guide on how to value an insurance agency - both in the sense of how a valuation agency/M&A advisor goes about valuation, and also in terms of what insurance agency owners can do to maximize their valuation prior to running an M&A deal.

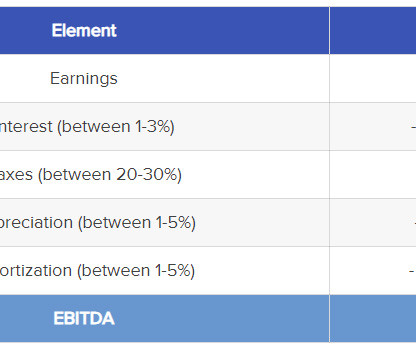

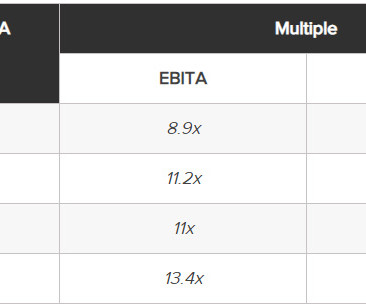

When insurance agency sellers have already met with prospective buyers, they may have been offered a valuation based on their “adjusted EBITDA.” The following article provides a brief overview of EBITDA and adjusted EBITDA valuations for insurance agencies. What Is EBITDA? What Is Adjusted EBITDA?

In today’s business landscape, mergers and acquisitions (M&A) are not just about profit and market share. Sustainability and ESG have become pivotal considerations in M&A deals, transforming how organizations evaluate, structure, and execute these transactions. These conditions can be included in the deal agreements.

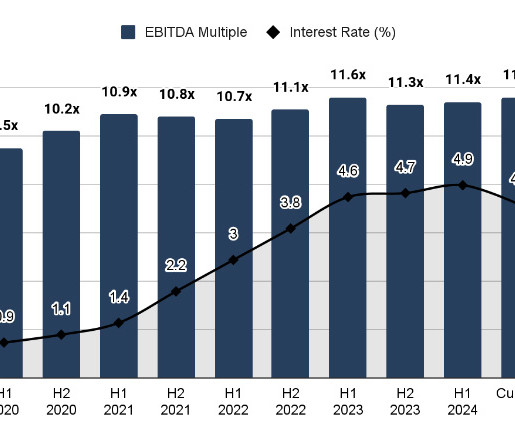

The inherent uncertainty of the M&A market over the last 18 months has underscored the importance of context for supplementing a full understanding before we can gain a better sense of what to expect in 2024. So, how did we get here? What Is Affecting Insurance Agency EBITDA Multiples?

established in 2017, has carved a niche in the market by specializing in manufacturing outdoor living and garden décor products. With a track record of over 400 successfully managed transactions across diverse industries, Sun Acquisitions is widely recognized as a leading M&A advisory firm in the Midwest.

We do not provide a detailed overview of the M&A process (readers can find this breakdown in " How To Sell: Insurance Agency M&A, Step-By-Step "), but focus instead on the changes specific to selling a family insurance agency. In particular, sellers should be aware of: Family Reputation as an Asset.

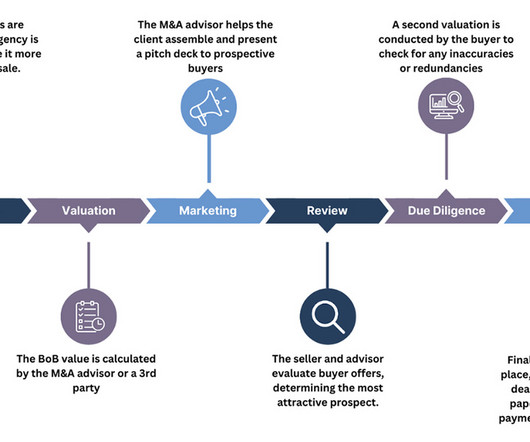

The following article details the process of selling an insurance agency book of business in 2024, including deviations from the process of selling an agency, the valuation process, and common payout structures. This means getting a formal valuation done - typically through your M&A advisor, but sometimes through a third party.

Since joining the firm in 2017, Tim has proven instrumental to its continued growth and the exceptional service the area’s leading middle market companies have come to expect from CCA. His track record of advising on more than 40 closed transactions totaling over $1.5 Tim holds a B.S. from the Robert H.

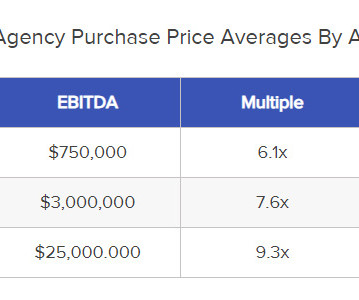

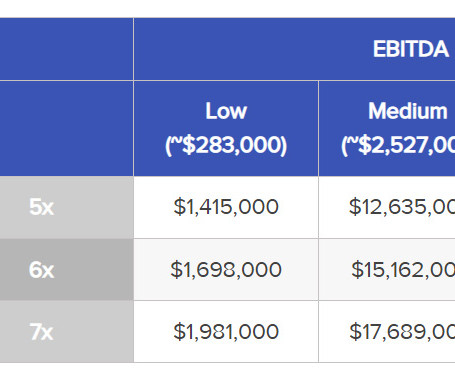

essentially boils down to three major steps: Determine your insurance agency’s EBITDA Determine the standard valuation multiple for an agency of your size Multiply your EBITDA by the multiple to determine your expected payout (i.e., Interest, taxes, depreciation, and amortization are then added to this number.

While we’ve already written extensively on the process of insurance agency valuation , the following sections focus on what to look for in the earliest stages of considering a sale - in other words, what deciding factors to look for to determine whether you should sell your agency. doesn’t have any strong succession prospects, or b.)

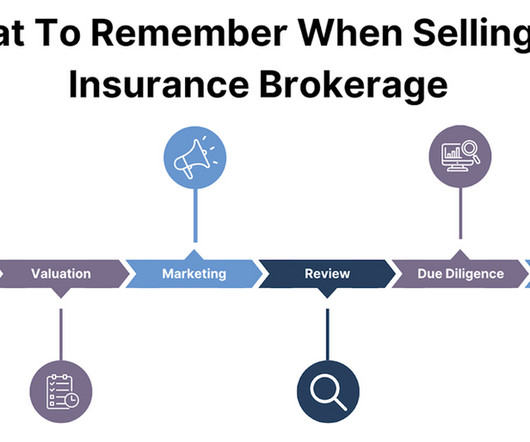

The Process of Selling an Insurance Brokerage Selling an insurance brokerage essentially consists of six phases and spans between 8-18 months on average: The Phases of Selling an Insurance Brokerage We should note that this process is longer than it used to be; insurance M&A transactions just a few years ago took between 6-12 months on average.

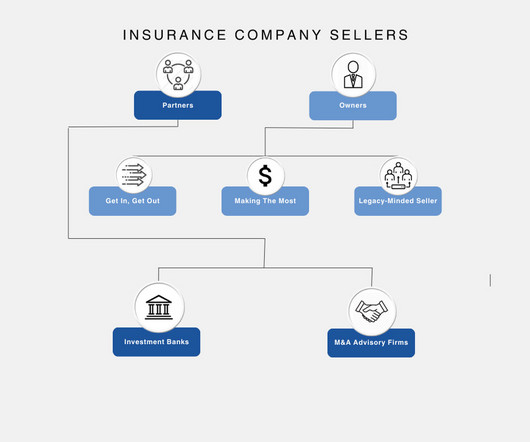

Seller 1: The Owners Insurance agency sellers typically have clear motivations and goals going into the M&A deal process. Insurance Agency Seller Motivations Insurance agency owners enter into an M&A arrangement with one of several goals in mind.

This was the fourth year in a row fundraising surpassed half a trillion dollars, with 2017, 2018, and 2019 recording the highest amounts of capital raised in history. This reflected the impact of valuations on deal flow and an increasing imbalance of potential sellers and buyers. The question is, “Why?”. Dry powder reached $1.4

In recent posts, we outlined the background of and reasons for the dramatic upsurge of private equity investment in the insurance brokerage industry , how the combination of private equity and low interest rates have dramatically raised valuations , and how private equity sponsored agencies increasingly dominate the insurance agency business.

To begin, we need to start with a few definitions: Investment Banks: We use the colloquial meaning of “investment banks,” which often includes M&A advisory firms and other financial services firms that facilitate the growth and sale of insurance agencies around a possible sale.

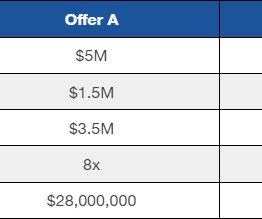

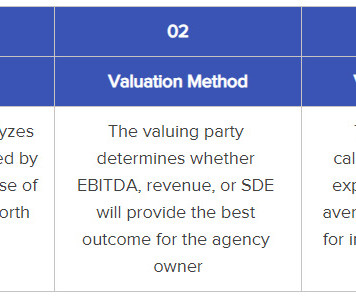

Let’s break down how this is paid: Valuation The valuation is invariably calculated as Pro Forma EBITDA multiplied by the EBITDA multiple. (Otherwise Known as “How Acquisitions Are Structured”) Our November blog post asked how a smaller agency can take advantage of the tsunami of private equity investment in insurance brokerages.

Similarly, sellers (particularly financial investors) in private M&A transactions are increasingly seeking the right to be able to monetize their rights to contingent consideration by requesting royalty-like earn-out streams and requesting a right to sell the potential future payments to a single third-party purchaser. Private placement.

M&A activity in physician practices continues to grow and outpace other sectors as deals in the healthcare industry are coveted by investors for their strong growth, recession resistance, and superior historical returns.

Historical Background Milestones One of the significant milestones of the WTO in the last decade includes the Trade Facilitation Agreement in 2017 , which aimed to simplify customs procedures, making trade cheaper and faster. The World Trade Organization (WTO ) plays a pivotal role in shaping the global economic landscape.

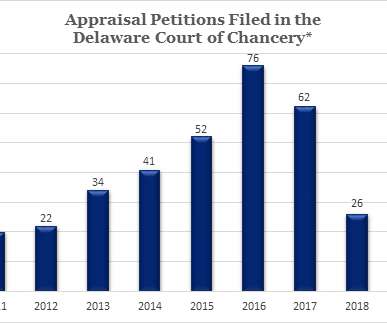

M&A practitioners have long advised boards of directors that the Delaware courts have never found that the events or circumstances in a particular transaction met the contractual standard of having a material adverse effect (or MAE) as defined in a merger or acquisition agreement. We can no longer give this advice. 2018-0300-JTL (Del.

M&F Worldwide Corp., M&F Worldwide Corp., In 2017, the Company began experiencing financial difficulty as it worked to update its flagship product, and in early 2018 it formed a special committee of its three independent directors to consider options for additional ways to raise capital. from the outset). 3d 635 (Del.

With extremely strong financial metrics, an excellent Rule of 40 ratio , and solid EBITDA , SEG agreed we were on the right track and guided us wisely through a process culminating in the transaction to Waud Capital in 2017. Our focus during this phase was on scaling the business through organic growth and an aggressive M&A strategy.

In a string of seminal decisions from 2017 through 2019 ( DFC Global , Dell and Aruba ), the Delaware Supreme Court re-shaped appraisal jurisprudence, in each case by overturning the Court of Chancery for failing to give adequate weight to deal price as the most reliable indicator of fair value. share, a 2.67% increase over the deal price.

Former stockholders of SARcode Bioscience were recently denied a claim that they were entitled to be paid $425 million in milestone payments under a merger agreement. The first milestone related to the outcome of a Phase 2 clinical trial of the drug in development to treat dry eye disease. Ultimately, the drug received regulatory approval.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content