This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What’s on tap for 2018 M&A? A recap of 2017 trends and the Cooley outlook on this year’s dealmaking: Buying Innovation: Retention and Non-Competes. As an example, for California specific requirements, see our prior blog post Non-Competes for California Employees in M&A Deals: Don’t Fudge It.

The following report examines the health and outlook for insurance M&A deals in 2024. We base this research on several key findings in our proprietary SF database, which observes and records data from the top ~400 insurance M&A buyers. Agency vs. Company: Which Is The Better Insurance M&A Deal?

2017-0032 (Del. M&F Worldwide, 88 A.3d M&F Worldwide, 88 A.3d Finding that "the controller announce[d] the conditions before any negotiations took place," the Court held the ab initio requirement was satisfied and dismissed the complaint under MFW. On February 2, 2018, Vice Chancellor J. 3d 635 (Del.

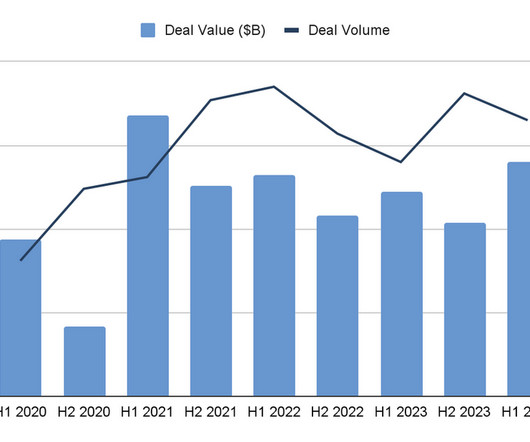

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

In it, we provide readers with a quick and simple overview of the current insurance brokerage M&A market , after which we discuss several macroeconomic and industry-specific factors that could drastically affect transactions in the next six months. The market is already highly competitive, but it’s also limited to what buyers can afford.

The insurance M&A market in 2024 is significantly more complex now than it was 20 years ago. However, this report seeks to make sense of these qualities as a whole to provide an overview of the 2024 insurance M&A market. The table of contents below offers quick links for readers seeking specific information in later sections.

On average, company leaders in any industry who attempt an M&A transaction using an in-house team average 30% less once the deal is complete. Below, we offer a basic breakdown of the most common advisors in an M&A transaction. The two most common types of M&A buyers are: Strategic. Retirement. Financial Security.

Compensation matters, including retention packages, equity treatment and related disclosure, are always key negotiating points in M&A transactions. In this post, we discuss compensation challenges in M&A deals in a depressed market and how dealmakers can address these issues.

government shutdown disrupting the market for IPOs, Brexit uncertainty, natural disasters and various other crises, cross-border M&A activity momentum continues. The following 10 key trends are underpinning hyperactivity in global M&A markets and are set to continue to shape deals well into 2019. In July 2018, the U.K.

2017-0032 (Del. M&F Worldwide, 88 A.3d M&F Worldwide, 88 A.3d Finding that "the controller announce[d] the conditions before any negotiations took place," the Court held the ab initio requirement was satisfied and dismissed the complaint under MFW. On February 2, 2018, Vice Chancellor J. 3d 635 (Del.

On August 18, 2017, Vice Chancellor Joseph R. Plaintiffs asserted that the sale was conflicted because Stewart negotiated for greater consideration for herself than for other stockholders and that the transaction did not meet the standards for application of the business judgment rule. M&F Worldwide, 88 A.3d 11202-VCS (Del.

Detailed below are our “notes from the field” for tech M&A in 2019. Tech M&A hit the global regulatory crosshairs in 2019 – creating a deal environment in which regulatory clearance, timing and scope of review quickly become one of the most critical factors in assessing transaction risk.

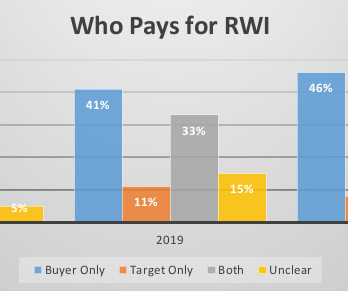

Goulston & Storrs M&A attorney Dan Avery is a nationally recognized expert on M&A deal point trends. The most recent three of these studies (2017, 2019 and 2021) have looked at representation and warranty insurance (“RWI”) in private company M&A transactions.

On August 18, 2017, Vice Chancellor Joseph R. Plaintiffs asserted that the sale was conflicted because Stewart negotiated for greater consideration for herself than for other stockholders and that the transaction did not meet the standards for application of the business judgment rule. M&F Worldwide, 88 A.3d 11202-VCS (Del.

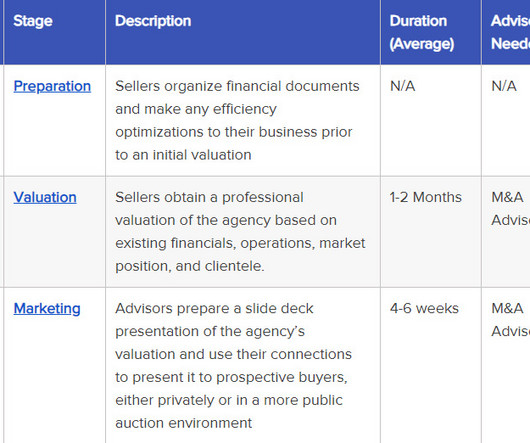

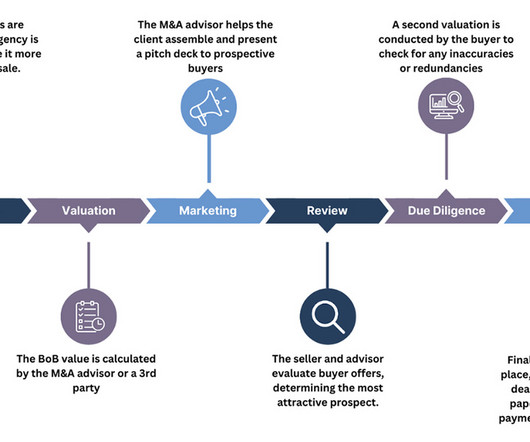

RIA valuations are typically performed by one of three parties: The M&A Advisor A Third-Party Specialist The Seller Themselves Although many sellers attempt to perform their own valuations, we strongly recommend against this. We highly recommend that sellers speak with an M&A advisor before taking their company to market.

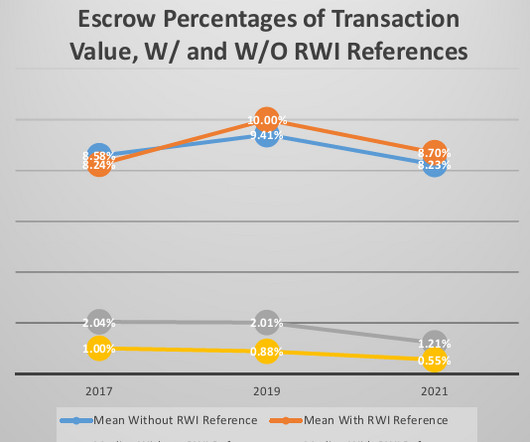

Goulston & Storrs M&A attorney Dan Avery is a nationally recognized expert on M&A deal point trends. This article examines trends relating to the use of indemnity escrows in private company M&A transactions. Typically, these escrows are held by a third party independent of the buyer and seller, such as a bank.

Goulston & Storrs M&A attorney Dan Avery is a nationally recognized expert on M&A deal point trends. The 2017, 2019, and 2021 ABA studies each show that indemnity caps were lower in reported deals where RWI was referenced in the deal documents, as compared with transactions without any such reference.

The wording of representations and warranties in a purchase agreement is critical, and ensuring their integrity is a vital role of the parties’ attorneys and, for the seller, their M&A advisor. In its survey, “2021 M&A Deal Terms Study,” SRS Acquion, Inc., six months) to long-term, perhaps as long as four years.

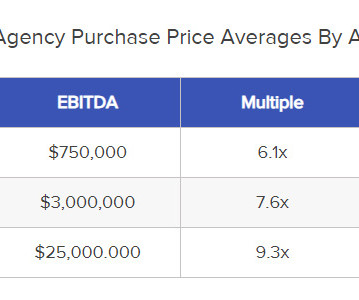

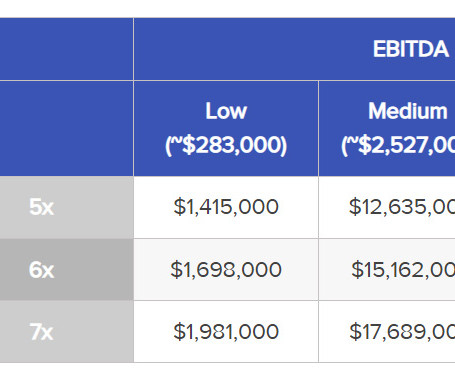

Insurance agency owners who are considering the prospect of running an M&A deal process often have many concerns about the fate of their agencies, but the most common by far are those surrounding the agency’s purchase price at closing. Some smaller agencies, for example, might get a higher multiple than 6.1x

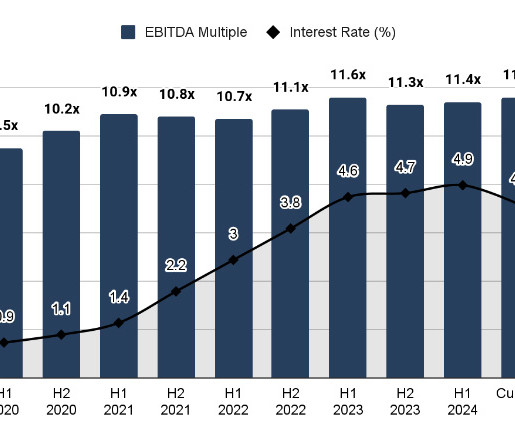

The Insurance Brokerage M&A Market in 2024 On average, insurance brokerages are seeing the highest valuations they’ve had in a decade. Until this happens, we expect the insurance broker M&A market to remain active but complicated. Since H1 2023, the average insurance brokerage valuation multiple has hovered around 11.6x

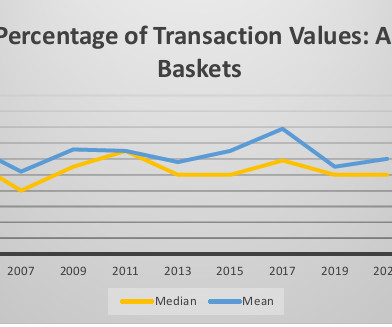

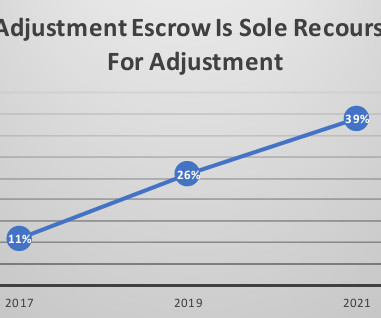

Goulston & Storrs M&A attorney Dan Avery is a nationally recognized expert on M&A deal point trends. In many M&A agreements with a purchase price adjustment, the parties agree to escrow a portion of the purchase price for a limited period following the closing. For example, on Jan.

For agency owners looking to sell their business in 2024, it’s helpful to know something about the insurance M&A buyer landscape before going in. The following section details the insurance M&A buyer landscape as of Q3 2024. To provide a sense of context for buyers’ current standing, we also include information from 2023.

This article presents a step-by-step guide on how to value an insurance agency - both in the sense of how a valuation agency/M&A advisor goes about valuation, and also in terms of what insurance agency owners can do to maximize their valuation prior to running an M&A deal.

Additionally, the court rejected buyer’s argument that it was permitted to terminate the transaction, finding that the target did not suffer an MAE and did not breach its conduct of business covenant, distinguishing this case from the court’s November 2020 opinion in AB Stable , which also involved a COVID-related M&A dispute.

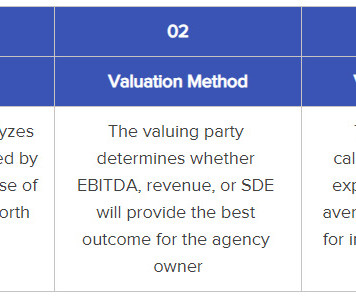

EBITDA: The Standard Insurance M&A Valuation Model EBITDA (Earnings before interest, taxes, depreciation, and amortization) is the standard valuation model within the insurance M&A industry. In addition, third-party M&A institutions like S&P Global Data or Statista can provide more generalized data.

This valuation model is used largely in M&A settings to determine the value of a company as it would appear to a prospective buyer by adding interest, taxes, depreciation, and amortization costs back into the business’s profits, since these elements will be fundamentally different post-closing. What Is EBITDA?

We do not provide a detailed overview of the M&A process (readers can find this breakdown in " How To Sell: Insurance Agency M&A, Step-By-Step "), but focus instead on the changes specific to selling a family insurance agency. In particular, sellers should be aware of: Family Reputation as an Asset.

Similarly, sellers (particularly financial investors) in private M&A transactions are increasingly seeking the right to be able to monetize their rights to contingent consideration by requesting royalty-like earn-out streams and requesting a right to sell the potential future payments to a single third-party purchaser. Private placement.

As one of the most active M&A firms in the insurance sector, we are frequently asked how insurance agency valuations work. This article discusses the fundamentals of insurance agency valuations, plus a few lesser-known factors that play into these processes before we give an overview of the insurance M&A market in 2024.

Consider Digitization Focus on Your Unique Selling Points (USP) Improve Client Retention Vet Prospective Clients & Carriers The Steps of Selling an Insurance Agency Book of Business Selling an insurance agency book of business shares all of the major steps of any M&A transaction and often involves the same team members.

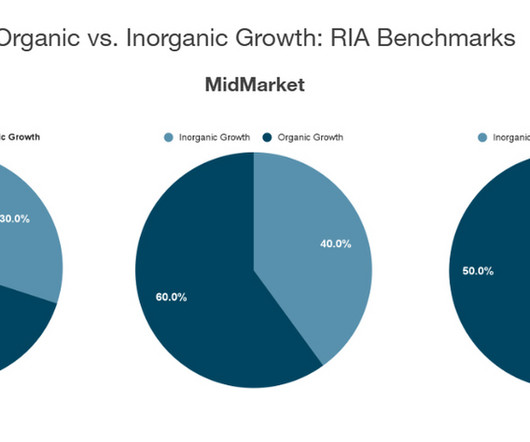

By Fee The following table outlines just a few key takeaways about various fee structures commonly found in RIAs as they apply to M&A transactions. RIA Fee Structures in M&A Because of the stability that is often associated with AUM fees, buyers tend to see RIAs with this payment structure as a more favorable prospect.

Legal Context The principle of freedom of contract, which allows sophisticated parties to freely negotiate the terms of their agreements and to rely on the enforceability of such agreements is a cornerstone of Delaware law. Specifically, in New Enterprise Associates 14 LP v. in the case of fraud). [3] in the case of fraud). [3]

M&F Worldwide Corp., M&F Worldwide Corp., In 2017, the Company began experiencing financial difficulty as it worked to update its flagship product, and in early 2018 it formed a special committee of its three independent directors to consider options for additional ways to raise capital. from the outset). 3d 635 (Del.

Remember the tumultuous acquisition attempt of Unilever by Kraft Heinz in 2017? Investment Bankers M&A advisory is replete with examples of retainer fees. While they're seen in numerous sectors, their significance shines particularly in investment banking , private equity, and corporate finance.

M&A practitioners have long advised boards of directors that the Delaware courts have never found that the events or circumstances in a particular transaction met the contractual standard of having a material adverse effect (or MAE) as defined in a merger or acquisition agreement. We can no longer give this advice. 2018-0300-JTL (Del.

M&A activity in physician practices continues to grow and outpace other sectors as deals in the healthcare industry are coveted by investors for their strong growth, recession resistance, and superior historical returns.

The court agreed with Gilead, based primarily on a review of the parties’ drafting and negotiating history, which was corroborated by the parties’ contemporaneous statements made after the European Commission approved the deal. for a Hematologic Cancer Indication.”

Former stockholders of SARcode Bioscience were recently denied a claim that they were entitled to be paid $425 million in milestone payments under a merger agreement. The first milestone related to the outcome of a Phase 2 clinical trial of the drug in development to treat dry eye disease. Ultimately, the drug received regulatory approval.

So far in the 2017 proxy season, ISS is almost universally recommending against all director elections at companies with a supermajority vote requirement to amend the company’s bylaws or charter, a classified board structure or a multi-class capital structure. in 2015 to 7.2% in 2015 to 7.2%

On June 27, 2017, the DE Supreme Court reviewed a net working capital adjustment and held that the buyer could not reopen the seller’s accounting methods by challenging the seller’s compliance with generally accepted accounting practices (GAAP) for purposes of the net working capital true-up. In Chicago Bridge v. Background facts.

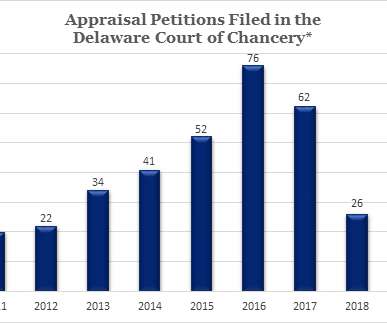

In a string of seminal decisions from 2017 through 2019 ( DFC Global , Dell and Aruba ), the Delaware Supreme Court re-shaped appraisal jurisprudence, in each case by overturning the Court of Chancery for failing to give adequate weight to deal price as the most reliable indicator of fair value. share, a 2.67% increase over the deal price.

6] The investors were provided with 8 pages of disclosure, which plaintiffs alleged was missing key material information, including information about the negotiations of the minority-approved independent manager and the Controller, and the fairness opinion received in connection with the squeeze-out merger. [7] in cash thereafter.

Leaks usually happen when there’s a stalemate in negotiations and can skew in the target’s favor in that the target may see a pop in its publicly traded price. In February 2017, TIF and JANA announced a cooperation agreement whereby Francesco Trapani (a key man here [9] ) and two others were appointed to the Board.

A major role of an M&A advisor is to help the seller keep their eye on that bigger picture, adds IBG managing partner John Johnson (Oklahoma). “We We are always alert to the tax aspects and, during the sale and negotiating process, will work to negotiate a structure that favors the seller. This is a timely concern.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content