This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It even includes elements of healthcare , industrials , and oil & gas investment banking. Real Estate: Data center, fiber, and cell tower REITs and potentially some healthcare REITs (e.g., In fact, a better question might be: What is NOT within the scope of infrastructure IB?

When you hear the words “healthcare private equity,” two thoughts probably come to mind: Wait a minute, isn’t healthcare a risky/growth-oriented sector? In most of the world, healthcare is either government-run or a mixed public/private sector. Are there many private healthcare companies for PE firms to acquire?

Many of these firms use debt to fund deals, and they complete bolt-on acquisitions for portfolio companies. Growth equity firms could invest in any industry but tend to be skewed toward technology and TMT , with some exposure to consumer/retail , healthcare , and financial services. What accounts for the difference?

In terms of industry focus , technology (especially “general IT,” Internet, and semiconductors) and healthcare have always accounted for a high percentage of deal activity. But you’ll also see manufacturing, cleantech, consumer, energy, real estate, and financial services deals.

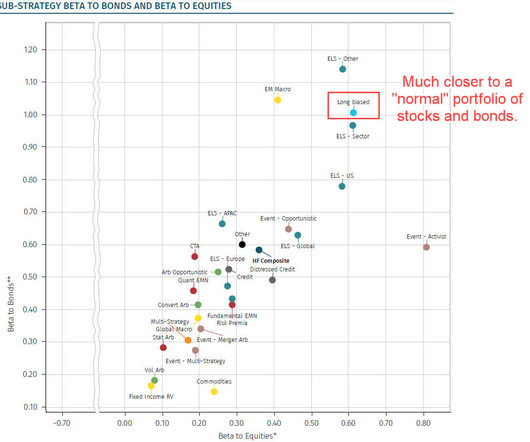

Also, many long-biased funds tend to have more concentrated portfolios since they often aim to become one of the top shareholders in each company. Think: a deep review of companies’ financial statements, 3-statement models , and DCF-based valuations. hiring MDs to analyze biotech companies).

Diversified Miners – These companies have a wide global portfolio of mines, and they extract, produce, and distribute just about every metal in the two categories above. One example is Steel Dynamics, which we feature in our main financialmodeling course. If you really like mining and want to specialize in it, sure, go ahead.

Portfolio Company Exits Does the parent company acquire many of the groups portfolio companies? FinancialModeling and Valuation: When you analyze a potential investment in CVC, you might look ahead to potential synergies if your firm ends up acquiring the startup in the future.

Its also much harder to find information on specific private credit deals, which may limit discussions about the firms portfolio and track record. For example, for many tech and healthcare companies, Intangible Purchases are the equivalent of CapEx and should arguably be part of the calculation.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content