This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Calculating cost of debt, cost of equity, and weighted average cost of capital (WACC). Enterprise Value = Market Capitalization + Total Debt - Total Cash. As we have previously covered what are needed to complete these steps in our DCF discussion , I would refer to those steps (1 through 7) here.

Market Capitalization Market capitalization is one of the simplest and most commonly used methods for valuing a publicly traded company. Example Scenario: Suppose XYZ Corp is a publicly traded technology company with 50 million shares outstanding, and the current share price is $20.

It can be useful for certain companies, such as power and utility firms and midstream (pipeline) operators in oil & gas … …but it’s also much harder to set up and use than a standard DCF. The basic set of steps looks like this: Step 1: Forecast Revenue and Expenses This is the same as in any other 3-statement model or DCF.

Thus far, we have covered four popular valuation methods in M&A (DCF, Comparable Company, Precedent Transaction, and LBO) and one less known one that is making its way out of the academic realm into the business world (Dividend Discount Method, DDM). TBV is calculated as follow: TBV = total assets - total liabilities - goodwill.

Infrastructure Investment Banking Definition: In infrastructure investment banking, bankers advise companies in the data center, renewables, transportation, utilities, and energy storage/transportation markets on equity and debt issuances, asset deals, and mergers and acquisitions. The difference in Midstream, at least in the U.S.,

By contrast, investment banking is more about advising companies on transactions such as M&A deals , equity and debt deals , and restructuring. You will very rarely get exposed to the type of financial modeling that bankers complete: 3-statement models , DCF models , M&A models , LBO models , and so on.

or debt offerings (investment-grade or high-yield bonds). Many firms put capital markets groups within “Investment Banking,” but some include it within Sales & Trading or “Global Markets.” You also pitch prospective clients on deals and spend time learning your industry.

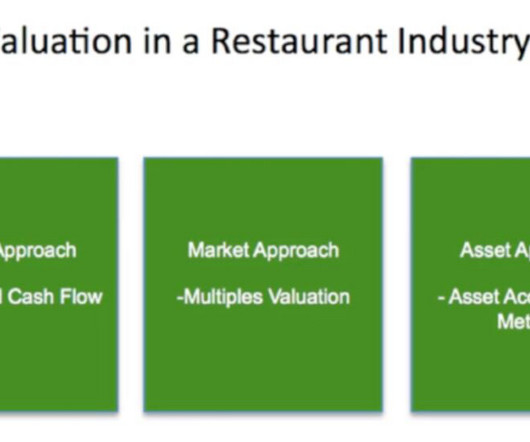

Below are the six recognized methodologies with short explanations of each: Discounted Cash Flow (DCF) Analysis: This analysis derives an ‘intrinsic’ value of a company. Essentially, comparable company analysis looks at the value of publicly traded companies. Comparable Company Analysis: This analysis provides “relative” valuation.

Mispriced Companies and Assets – Some mature healthcare firms trade at low valuation multiples , often because the market misunderstands their contracts, revenue, or track record. PE firms view these companies as especially appealing since low multiples mean they can use higher debt percentages to fund the acquisitions.

Non-Equity Funds – Finally, it is difficult to “short” certain securities effectively, such as distressed debt and many types of credit (especially structured products ). Think: a deep review of companies’ financial statements, 3-statement models , and DCF-based valuations. hiring MDs to analyze biotech companies).

Metals & Mining Investment Banking Definition: In metals & mining investment banking, professionals advise companies that find, produce, and distribute base metals, bulk commodities, and precious metals on debt and equity issuances and mergers and acquisitions. What Do You Do as an Analyst or Associate in the Group?

Traditionally, banks gave away equity research reports for free to incentivize large clients to trade with the bank. Therefore, equity research generated revenue indirectly via trading commissions , but it was still considered a front-office role due to the compensation, interaction with managers and investors, and exit opportunities.

billion market cap that trades at 7x trailing revenue on expected revenue growth rates of 15 – 20% and projected EBITDA margins of ~20%. A: Unlike most PE deals, traditional growth equity deals do not use debt and are for minority stakes in companies, but they often have more “structure” via liquidation preferences and preferred stock.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content