This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Summary of: What Privacy, Security, and Compliance Documentation Will Acquirers Expect? In this article, well outline the key privacy, security, and compliance documentation that buyers especially private equity firms and strategic acquirers expect to see during due diligence.

Summary of: M&A Advisory for SaaS Businesses Under $50 Million: Strategic Considerations for Founders For founders of SaaS companies generating under $50 million in revenue or enterprise value, the M&A landscape presents both opportunity and complexity. Strategic vs. Financial Buyers: Whos the Right Fit?

If it makes financial sense and you understand the dilution aspect of selling equity and the potential interference from investors, then yes, go ahead. In this post, we’re going to address what these are, some of the challenges to expect, how to sell the equity, and who to sell it to. Selling equity – the good, the bad, the ugly.

Selling or growing your business requires careful preparation, the right advisory team, and strategic foresight. Financial Buyers : These are typically investment companies, such as private equity firms, with no prior investment in your industry. Legal : Corporate documents, legal issues, compliance with regulations.

By Dom Walbanke on Growth Business - Your gateway to entrepreneurial success Raising private equity funds is seen as the holy grail for businesses who want to grow quickly, simply because the strength of capital opens the door for rapid growth.

In the world of mergers and acquisitions, the Confidential Information Memorandum (CIM) is more than just a document its your companys first impression to serious buyers. A CIM is a detailed, confidential document prepared by a company (or its M&A advisor) to present the business to potential acquirers or investors.

Private equity (PE) firms are investing in middle market businesses at a healthy pace despite a high interest rate environment that makes it more costly to finance deals. In return, you will agree to roll over as much as 20-35 percent of the deal value as equity in the new business. Your EBITDA is in the range of $1M – $5M.

But in nearly all cases, the quality and clarity of your financial documentation will directly impact valuation, deal structure, and buyer confidence. Buyers whether strategic acquirers or private equity firms will typically expect at least GAAP-compliant financials. What Financial Documentation Are You Overlooking?

Key Considerations Before Buying In: Equity and Ownership : Determine what percentage of the business you’re acquiring, as it will influence your role in decision-making, profit distribution, and overall control within the company. Defining Your Level of Involvement Decide if you want to be hands-on in operations or prefer an advisory role.

The transaction – first reported on back in April – was previously valued at £410 million according to documents seen by The TRADE. Deutsche Numis is set to serve more than 170 corporate broking clients and is focused on providing comprehensive financial and advisory solutions.

Why Open Source Raises Red Flags in M&A Buyers particularly strategic acquirers and private equity firms are increasingly cautious about open-source software (OSS) usage. How to Prepare for Diligence: A Strategic Checklist To avoid surprises during due diligence, founders should proactively audit and document their open-source usage.

Key Drivers of Software Company Valuation Buyerswhether strategic acquirers or private equity firmsevaluate software companies through a combination of financial, operational, and strategic lenses. appeared first on Transforming Tech: The Premier M&A Advisory Firm for Software and Technology Businesses.

New global studies of both suggest that heightened private equity interest will see deal rates maintain higher levels in the coming year, too. Equiteq is an international provider of strategic advisory and M&A services to consulting firms and the broader knowledge economy.

Whether your firm fits in this category can affect how you approach potential buyers, from strategic acquirers to private equity groups. As for documentation: Financial Statements: Past three to five years of income statements, balance sheets, and cash flow statements. What Post-Sale Considerations Should I Keep in Mind?

But with the right preparation and advisory support, the timeline can be managed strategically to align with your goals whether thats maximizing valuation, minimizing disruption, or closing before year-end. Due Diligence & Closing (23 months): Legal, financial, and technical diligence, followed by final documentation and closing.

a strategic legal advisory out of New York City, is a prime example of someone who has been successful in this field. His advisory practice helps them through catalytic, transformational, and strategic events, such as mergers and acquisitions, governance issues, capital raising, and disputes.

Prepare the Business for Sale Buyers especially private equity firms and strategic acquirers expect a clean, well-documented business. Operational Documentation: Create SOPs, org charts, and product roadmaps to reduce perceived risk. Rollover Equity: Retaining a stake in the new entity, common in private equity deals.

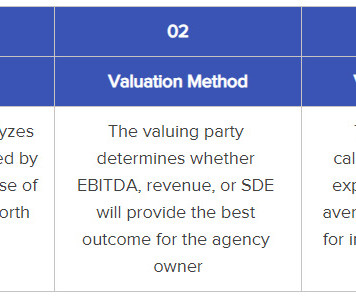

The following article discusses how to value a Registered Investment Advisory firm (RIA) prior to taking it to market. These documents include: How To Value an RIA: Key Documents by Type Sellers should be prepared to have their M&A advisor or a third party (usually provided by the advisor) review these documents in detail.

And it certainly does not stop less-than-reputable advisory firms from agreeing to represent you and taking their regular retainer fees, despite knowing full well your agency can’t be sold. What Documents Do I Need? Beyond proof of sustained profitability when analyzing these documents, look for: Liquid Assets. Manageable Debt.

A closing binder (also called a closing book) is a comprehensive, organized collection of all final, executed documents related to the acquisition. What You Need Ready Before Closing By the time you reach the closing table, most of the heavy lifting due diligence, negotiation, and documentation should be complete.

Your answers will shape the type of buyers you target from strategic acquirers to private equity firms or growth investors. litigation, debt) are disclosed Team & Org: Document key roles, retention plans, and any dependencies on founders or key personnel Many founders underestimate the time and effort required here.

A term sheet is a document that outlines the terms of a proposed transaction. If the document functions like an IOI, it may only provide a range of valuations. Rollover equity : When private equity buyers want you to roll a percentage of your proceeds into equity, there’s often a lot of back and forth.

The late 2010s, however, saw an explosion of private equity activity that has dramatically increased that pool from 5 to more than 50. Financial: Often referred to as private equity, these buyers are interested in purchasing an insurance agency for the express purpose of making it more profitable and then reselling it further down the road.

The following table contains a comprehensive list of the documents our teams use to value an insurance agency. How To Value an Insurance Agency: Required Documentation Your M&A advisor will use these documents to value your agency, as detailed in the sections below. Contact us to discuss a future partnership.

Buyersespecially strategic acquirers and private equity firmsare not just purchasing code; theyre acquiring the legal rights to use, commercialize, and defend that code. IP Hygiene as a Value Driver Beyond risk mitigation, clean IP ownership and documentation can actually increase your companys valuation.

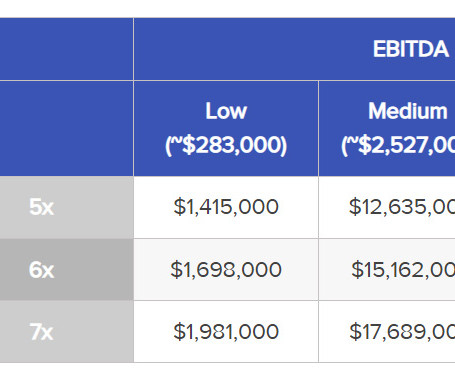

The shortest answer we can give is, “You give us some specific documentation, and we’ll run some numbers to determine how much the agency is worth.” Our data has shown a 30% increase in deals that feature equity as a larger portion of the seller payout since 2018. There are surprisingly few large insurance brokerages.

rn In the podcast, Chelsea Mandel, the founder of Ascension Advisory, discusses her experience in the real estate and M&A space, particularly in sale-leasebacks. This strategy involves a business, private equity owner, or sponsor selling its company-owned real estate that is considered mission-critical to its operations.

Kirk Michie, with his three decades of experience in finance and business advisory, has honed his expertise in mergers and acquisitions, making him well-suited to assist entrepreneurs in navigating these transactions. The podcast also touches on the importance of accurate financial records and documentation in business transactions.

This usually leads to equity-based payouts. private equity firms, investment banks, individual investors). The advisory team targets a single high-profile buyer on whom they focus their marketing efforts. The owner wants to maximize the transaction’s payout. A Quick Turnaround. Account-Based.

Culturally, the company DNA was solid; the development team maintained thorough documentation and executed on its plans. The company didn’t have a board of directors or a formalized advisory board, which isn’t uncommon for early-stage companies, but as CPFD matured, it lacked senior professionals who could provide growth expertise.

In our experience at iMerge, companies that proactively document and defend these attributes tend to command higher multiples and face fewer hurdles during due diligence. Neglected Documentation: Lack of technical documentation, version control, or audit trails can reduce buyer confidence.

Buyers whether private equity firms, strategic acquirers, or growth investors are not just buying code. This allows time to clean up financials, resolve legal gaps, and document key processes. Document Tech Stack: Provide a clear architecture overview, third-party dependencies, and any known technical debt.

This article outlines the key tax and legal documents you should be prepared to manage after selling your software or technology business, with a focus on the months following the transaction close. Recordkeeping and Audit Preparedness Even after the deal closes, you should retain all transaction-related documents for at least seven years.

Identify and reach out to potential buyers, which could be competitors, financial investors (private equity firms), or firms in adjacent sectors. This involves providing detailed financials, legal and operational documentation and data, answering queries, and showcasing the genuine potential of your technology assets.

Key Drivers of Software Company Valuation Buyerswhether strategic acquirers or private equity firmsevaluate a range of quantitative and qualitative factors. Document IP and contracts : Ensure all software code, licenses, and customer agreements are properly documented and assignable. Here are the most influential: 1.

One strategy for moving forward in a merger of equals transaction is to agree on a timeline for aligning on key issues and then only move to drafting definitive documents once the key issues have been agreed. Like in an equity financing transaction, the combined company will often establish a new go-forward equity pool.

In reality, buyersespecially private equity firms and strategic acquirersexpect a well-documented, diligence-ready business. appeared first on Transforming Tech: The Premier M&A Advisory Firm for Software and Technology Businesses. IP ownership: Unclear or incomplete IP assignment from early contractors or developers.

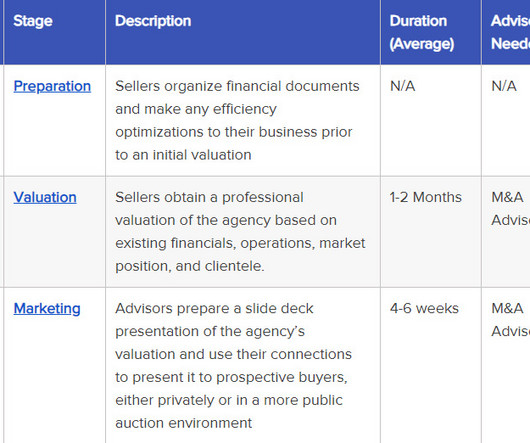

Changes in the Valuation Process Valuation is the first formal step in the M&A deal process, taking place once the seller has gathered all their preliminary documents and made any necessary changes to the company's internal structure to make it more profitable. Family-specific financial arrangements.

For example, if your SaaS platform dominates a specific industry vertical and is being acquired by a competitor or a private equity firm with a roll-up strategy in that space, the deal may attract scrutiny. With the right advisory team, you can navigate these hurdles confidently and keep your deal on track.

It’s exciting when a private equity investor or strategic buyer shows interest in your company, but it’s essential not to get carried away, especially early in the courting process. Guidance from an M&A Advisor : Your advisory team will typically oversee this intricate process for you, given its complexity.

Private equity firms Especially those executing roll-up strategies in vertical SaaS, infrastructure software, or B2B marketplaces. For example, a strategic acquirer may prioritize product integration and offer a higher upfront price, while a PE firm may emphasize recurring revenue and prefer earn-outs or equity rollovers.

Even after months of diligence, negotiation, and documentation, the final 5% of the deal often requires 50% of the effort. These agreements can become sticking points if compensation, non-competes, or equity rollover terms are not aligned with expectations. In founder-led businesses, key person risk is a major concern.

The SEC’s fellow domestic regulator, the Commodity Futures Trading Commission, also let the market know this summer through an advisory that some prime brokers may have to register as derivatives clearing organisations (DCOs), in what could be a burdensome process.

Consult your own documents when making these calculations, and use the examples in this article only as a template. That number is often complicated by what percentage of your payout is cash vs. equity, the timeline in which it is paid out, and additional considerations like post-closing employment agreements or milestone earnouts.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content