This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

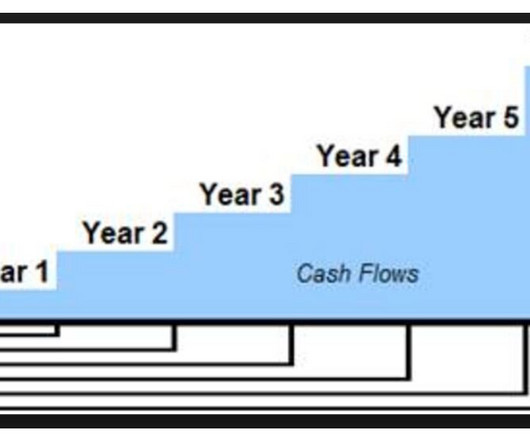

As I mentioned in my last post, DiscountedCashFlow (DCF) is a valuation method that uses free cashflow projections, a discount rate, and a growth rate to find the present value estimate of a potential investment. It is worth noting that each step can justifiably warrant an entire post in itself.

The discountedcashflow analysis, commonly referred to as the DCF, along with the Leverage Buyout Analysis, commonly referred to as the LBO, are some of the most commonly used and complex financial modeling techniques on the Street today.

If you don’t have an account already, create a free account here and purchase our Buyside Starter Kit with the code BUYSIDESTARTER here. A Few Reads to Digest Valuation Simplified: How DiscountedCashFlow Modeling Drives Financial Analysis Harness DiscountedCashFlow (DCF) modeling for financial analysis.

Adjust for Differences: Make necessary adjustments to account for differences between the target company and the comparables, such as growth rates or profit margins. The underlying principle is that the value of a business is equal to the present value of its expected future cashflows, taking into account the time value of money.

When considering buying an existing business, it is important to take into account the size of the business. However, it is important to take into account the size of the business and to understand the process of buying an existing business. Finally, experienced employees can provide valuable insight and knowledge to the business.

Valuing a company that operates in a highly volatile industry with unpredictable revenue streams and market conditions requires a thoughtful approach that takes into account the unique characteristics and risks associated with the industry. Use different discount rate scenarios to account for varying levels of risk and uncertainty.

Terminal Value The terminal value is an essential component of a discountedcashflow (DCF) analysis. It represents the value of a business or an investment beyond the explicit projection period used in the DCF model. Here are three widely used approaches: 1.

Evaluate Valuation Methods: Select appropriate valuation methods that account for the impact of inflation and currency fluctuations. DiscountedCashFlow (DCF) models can be adjusted by incorporating inflation rates and currency exchange rate assumptions into cashflow projections.

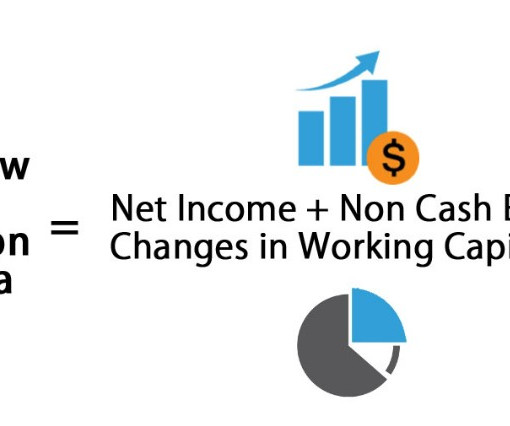

Diving Deep into CashFlow from Operations Cashflow from operations is calculated by adjusting net income for non-cash expenses and changes in working capital. Net Income - It's the starting point for calculating CFO, but it's based on accrual accounting.

DCF: DiscountedCashFlow Estimates a company’s value and forecasts future cashflow by incorporating the time value of money. DCF is used when making investment decisions and understanding a business’s current and future value. CAGR can be used to compare your performance against industry averages.

Still another potential problem is that sometimes we must use public company data and then discount the results because the subject company is private. To account for this variability, valuation professionals will lean into the comparables they feel are closest and most accurate and discount or remove entirely those that seem unrealistic.

Below are the six recognized methodologies with short explanations of each: DiscountedCashFlow (DCF) Analysis: This analysis derives an ‘intrinsic’ value of a company. This means that the method evaluates the future cashflow of the company and then discounts those cashflows to the present day.

As opposed to merely focusing on the market capitalization, which only accounts for the company’s equity value, the Enterprise Value Calculator considers the company’s debt, cash, and other financial liabilities. EBITDA multiples allow you to assess a company’s earnings power and its ability to generate cashflows.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content