This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Few companies divest units immediately following an acquisition (unless they are compelled to do so by antitrust regulators), but many companies divest them eventually. In any given year, nearly half of the acquisitions that occur come about because the sellers are divesting a company unit. Recent U.S. examples include Sara Lee Corp.’s

The board has consciously decided to pursue a strategy that includes inorganic growth through strategic acquisitions that can help move the company's growth forward. The implications of this acquisition will be substantial for Virtualware and the industry. euros per share, up 40% from its initial IPO price of 6.00

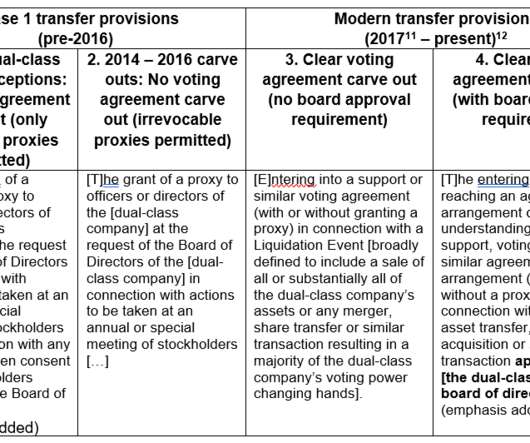

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders. Potential carve outs for M&A voting agreements.

bakery market has shown steady historical growth, with industry revenue rising roughly 4% annum from 2004 to 2022. Selling majority ownership but not 100% to a PEG allows the owner to take significant funds off the table, while securing growth capital to invest in automation, operational enhancements, and further acquisitions.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content