This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To be fair, in some industries – like commercial banks and insurance within FIG – the DDM is a core valuation methodology. It can be useful for certain companies, such as power and utility firms and midstream (pipeline) operators in oil & gas … …but it’s also much harder to set up and use than a standard DCF.

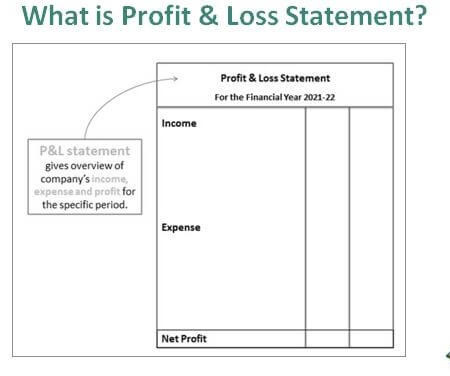

A profit and loss (P&L) statement, sometimes called as an income statement, is a financial report that provides investors and outsiders with a financial overview of a company. The P&L outcome plotted on a trendline assists investors in understanding the organization’s performance over time.

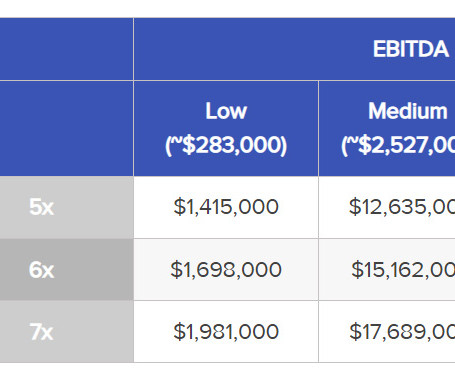

When insurance agency sellers have already met with prospective buyers, they may have been offered a valuation based on their “adjusted EBITDA.” The following article provides a brief overview of EBITDA and adjusted EBITDA valuations for insurance agencies. What Is EBITDA? What Is Adjusted EBITDA?

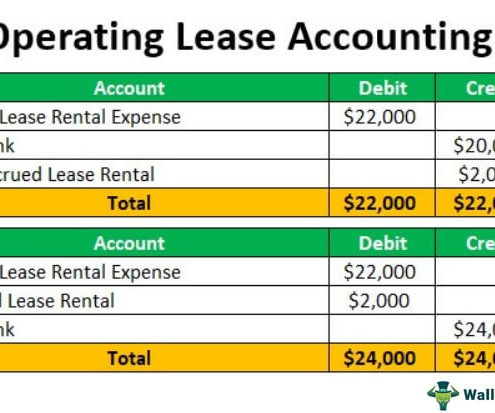

At the same time, the lessee utilizes the asset for an agreed period, known as the lease term. Unlock the art of financial modeling and valuation with a comprehensive course covering McDonald’s forecast methodologies, advanced valuation techniques, and financial statements.

essentially boils down to three major steps: Determine your insurance agency’s EBITDA Determine the standard valuation multiple for an agency of your size Multiply your EBITDA by the multiple to determine your expected payout (i.e.,

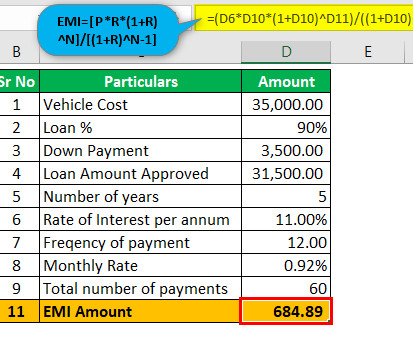

About Loan [P*R*(1+R)^N]/[(1+R)^N-1] Wherein, P is the loan amount R is the rate of interest per annum N is the number of period or frequency wherein loan amount is to be paid Loan Amount (P) The loan Amount $ ROI per annum (R) Rate of Interest per annum % No. How to Calculate? Each of such points cost 1% of the loan amount.

I started with my monthly after-tax salary and, from there, subtracted necessary expenses such as rent, utilities, and other reoccurring expenses. When it came to funding business school, I did so by liquidating a portion of my investments (which were mostly in S&P index tracker funds), as soon as I made the decision to pursue an MBA.

4) Flow: Connect the Statements Create the cash flow statement by linking your Balance Sheet and P&L. Roll forward the Balance Sheet using the P&L and Cash Flow. c) Utilize macros to create interactive dashboards and scenarios. You'll be amazed at how much faster and efficient you become.

One way to ensure that the client is getting the best results from their marketing efforts is to focus on the entire P&L of the company. This means that businesses should be looking at their COGS, distribution, and other factors that go into their P&L to get a better understanding of how the business is running.

PE firms rely on leveraged buyouts (LBOs) for the lion's share of their deals, which often involve using the acquired company’s assets as collateral to insure the loan used to purchase it. Conversely, when interest rates are high, valuations are supposed to decrease because buyers will try to make up what they are losing to interest.

The metals & mining team’s classification varies based on the bank. Sometimes, it’s in the broad “Natural Resources” group, but it could also be in Industrials , Renewables, or even Power & Utilities. Valuation , such as the different multiples used for mining companies and the NAV model in place of the DCF (see below).

As the quote from Warren Buffett above suggests, we share his view on the utility of short-term market forecasts. Equities and the S&P 500 At the onset of each new year, like clockwork, we’re asked for our near-term view. benchmark equity index, the S&P 500. This year was no different.

E247: Why Accurate Financials are Key to Success in Buying, Selling, and Valuing Businesses - Watch Here About the Guest(s): Ryan Hutchins is an accomplished entrepreneur and expert in the field of mergers and acquisitions. Under his leadership, the company has grown exponentially, conducting over 1,400 valuations annually.

Uncovering the Secrets of E-Commerce M&A with Justin Harris - Watch Here rn rn About the Guest(s): rn Justin Harris is a seasoned expert in mergers and acquisitions with a strong focus on the website and e-commerce space. rn rn rn Utilizing AI for generating sales copy and content can be a game-changer for small e-commerce businesses.

Business owners who lacked longstanding relationships with creditors found themselves without many options, and forced to utilize distressed debt and special situations funds. COVID-19’s impact on M&A activity varied across industries, with some reaping the benefits and others not being so lucky. of debt capital raised in 2019 [9].

While 2020’s M&A landscape was characterized by whiplash volatility from choppy deal activity in the first half of the year to a surge in volume in the second half, that momentum accelerated in 2021, with no signs of slowing down heading into 2022. on transactions over 2019’s mega?mergers. General trends in life sciences M&A.

Government funded programs include Medicare, Medicaid, Children’s Health Insurance Program, and the Veterans Health Administration. The key issue is that most businesses in this subsector started off as one-product companies and raised large amounts of capital without considering clinical utility and economic benefits.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content