This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Access to credible sources of information such as SEC EDGAR database , Treasury.gov , OECD GDP Forecast , Mergent Online, S&P Capital IQ, Hoovers, ValueLine, Yahoo Finance , MarketWatch , and Damodaran Online. Inexpensive Excel-plugin simulator such as @RISK are available for download online.

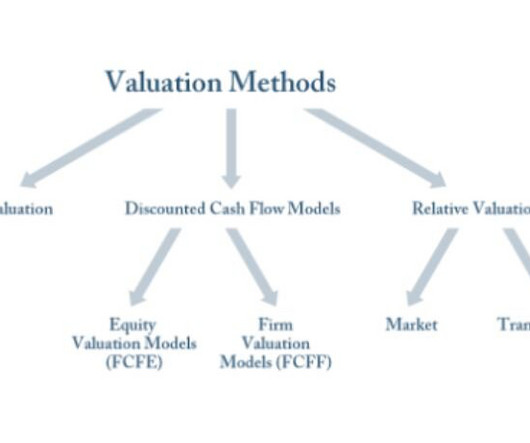

It has been roughly three years since my last blog post at the completion of my fellowship. To pick up where we last left off with valuation, I will cover the topic of a Merger Relative Valuation in this blog post and move on to other non-valuation topics from here. Time certainly did fly by when one was having fun.

Once the extraordinary, unusual, non-recurring items are identified, the next (2nd) step is to have them added back / removed from the historical income statement to normalize the financialstatement. Expense items are added back and gain items are removed.

Regardless of the base reason(s), the current owners and management of a company looking for a new owner should seek to: Maximize return on investment for current owners. In an earlier M&A post, we have discussed how private companies’ accounting statements differ from public companies’.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content