This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As I mentioned in my last post, Discounted Cash Flow (DCF) is a valuation method that uses free cash flow projections, a discount rate, and a growth rate to find the present value estimate of a potential investment. Calculate cost of debt, cost of equity, and weighted average cost of capital (WACC).

On August 1, 2017, the Delaware Supreme Court, in an opinion by Chief Justice Leo E. Strine, Jr., reversed and remanded an appraisal ruling that had determined the buyout of DFC Global Corporation ("DFC") by private equity investor Lone Star at $9.50 per share significantly undervalued the stock of DFC. DFC Global Corp. per share, 8.4%

Liabilities represent the obligations a company has to outside parties, such as debts, loans, and accounts payable. For example, Amazon's acquisition of Whole Foods in 2017 required careful analysis of the accounting equation to determine the financial impact of the transaction. For example, Apple Inc. reported total assets of $338.16

On August 1, 2017, the Delaware Supreme Court, in an opinion by Chief Justice Leo E. Strine, Jr., reversed and remanded an appraisal ruling that had determined the buyout of DFC Global Corporation ("DFC") by private equity investor Lone Star at $9.50 per share significantly undervalued the stock of DFC. DFC Global Corp. per share, 8.4%

This was the fourth year in a row fundraising surpassed half a trillion dollars, with 2017, 2018, and 2019 recording the highest amounts of capital raised in history. This reflected the impact of valuations on deal flow and an increasing imbalance of potential sellers and buyers. PE-backed deal flow declined somewhat in 2019.

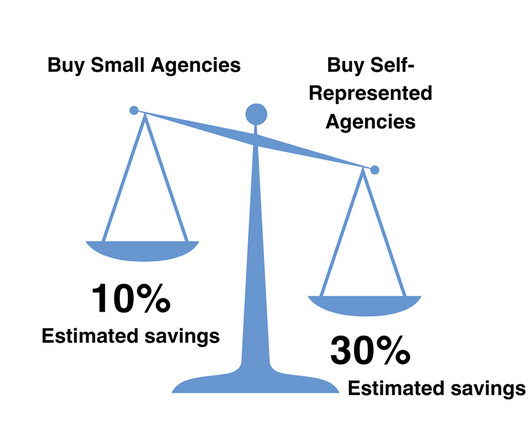

In addition to the high cost of debt interfering with their bottom line, they also have to contend with a buyer pool that’s larger than ever before , with 50+ buyers in the current pool where there used to be ~5. Sellers are remaining patient and working with M&A advisosr to identify areas of opportunity.

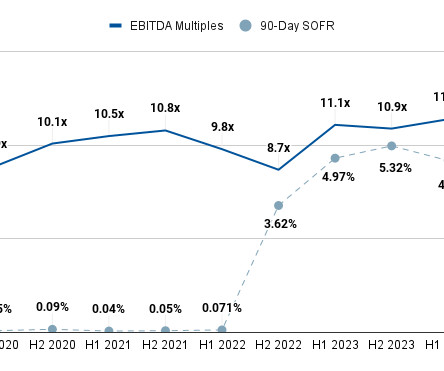

Conversely, when interest rates are high, valuations are supposed to decrease because buyers will try to make up what they are losing to interest. PE Cost of Debt vs. RoR, H1 2020 - H2 2023 This inverse spread indicates one of the strongest seller’s markets we’ve seen in the insurance M&A market to date. for insurance agencies.

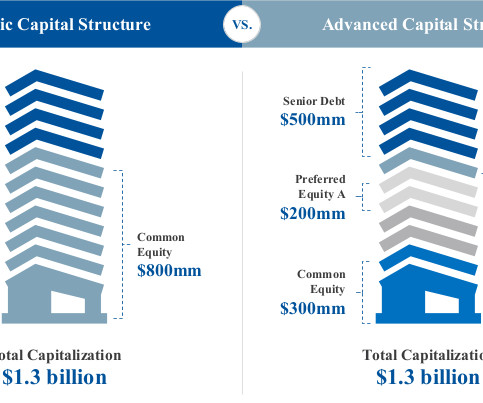

While the cost of debt has increased to the point that buyers often acquire brokerages at an initial loss, insurance brokerage M&A multiples have not only held steady but are actually seeing all-time highs. Equity used to consist of senior debt (i.e., the amount all common shareholders invest in the brokerage).

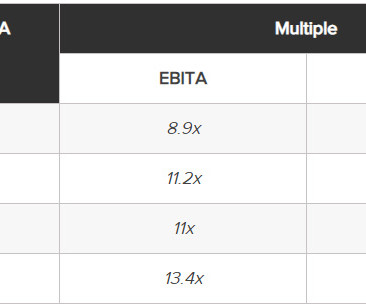

Starting in H2 2022, the insurance M&A market has seen a notably difficult 18-month period, afflicted with high interest rates, lowered deal volumes, and lowered valuations. If they do, then we can expect to see valuations and, by extent, EBITDA multiples for insurance agencies rise. Learn more at , ,, SicaFletcher.com.

Other times, they are hoping to use their share of the sale to alleviate personal debt. Once you get into the valuation stage (which is usually done by your M&A advisor or a 3rd party valuation agency), you will need a large swath of documentation. Manageable Debt. Are looking for a career change.

Financial Modeling & Valuation Courses Bundle (25+ Hours Video Series) –>> If you want to learn Financial Modeling & Valuation professionally , then do check this Financial Modeling & Valuation Course Bundle ( 25+ hours of video tutorials with step by step McDonald’s Financial Model ).

In recent posts, we outlined the background of and reasons for the dramatic upsurge of private equity investment in the insurance brokerage industry , how the combination of private equity and low interest rates have dramatically raised valuations , and how private equity sponsored agencies increasingly dominate the insurance agency business.

essentially boils down to three major steps: Determine your insurance agency’s EBITDA Determine the standard valuation multiple for an agency of your size Multiply your EBITDA by the multiple to determine your expected payout (i.e., Learn more at SicaFletcher.com.

Since H2 2022, industries across the board (including insurance) have seen declines in deal volume as prospective buyers have withheld their funds for more favorable conditions in which the cost of debt is not so high. It is possible that deal durations may decrease if interest rates are lowered; however, this is no guarantee.

personal debt, business/legal liabilities, time-sensitive investment opportunities) may prompt owners to sell quickly. Your agency valuation will play a large role in influencing how buyers perceive your agency’s worth. Financial Need. Urgent financial requirements (e.g., Market/Business Environment. Learn more at SicaFletcher.com.

In-depth analysis that might take days or weeks, such as a financial model with 1,000 rows in Excel to assess a biopharma company’s valuation. This is especially common in areas like distressed debt investing that depend heavily on catalysts. Putting out fires” when emergencies arise, such as unexpected company announcements.

Capital is available, valuations have started to normalise and the debt markets are still supportive – albeit with greater scrutiny and higher costs. The data below from Statista shows the volume of UK private equity deals between 2017 and 2022. They helped to build trust, mutual respect and a shared vision of the future.

The transition away from Libor began in earnest in 2017, when regulators raised concerns about the reliability and integrity of the benchmark. The regulation also led to changes in risk management practices and valuation methodologies for financial institutions.

Infrastructure Investment Banking Definition: In infrastructure investment banking, bankers advise companies in the data center, renewables, transportation, utilities, and energy storage/transportation markets on equity and debt issuances, asset deals, and mergers and acquisitions.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content