This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

UK & European Financial Services M&A: Sector trends H2 2022 | H1 2023 — Fintech - Whilst many European start-ups have struggled to successfully execute funding rounds at valuation levels of yesteryear, more mature fintechs have pivoted to acquisitions and partnerships to fuel growth.

Financial terms of the deal, which marks Stripe’s first acquisition since it bought card reader provider BBPOS in January of 2022, were not disclosed. It was while pitching Stripe in 2022 that the small startup “really hit it off with the engineering leaders, and “from there, it evolved into more of an acquisition discussion,” said Boulander.

Posted by Ian Nussbaum, Bill Roegge, and Meredith Klionsky, Cooley LLP , on Wednesday, October 19, 2022 Editor's Note: Ian A. Nussbaum is a partner, Bill Roegge and Meredith Klionsky are associates at Cooley LLP. This post is based on a memorandum by Mr. Nussbaum, Mr. Roegge, Ms. Klionsky, and Mr. Nimetz.

Posted by Christopher M. Noel, Skadden, Arps, Slate, Meagher & Flom LLP, on Wednesday, October 12, 2022 Editor's Note: Christopher M. SPAC activity continued to slow in the first half of 2022, a sharp decline from the number of deals and IPOs in the same period in 2021. Michael Chitwood, and Gregg A.

On the latest episode of The Deal’s Behind the Buyouts podcast, Solomon Partners co-head of consumer and retail Cathy Leonhardt talks about the sector’s slow start to M&A this year, categories that continue to shine and potential signs of a resurgence in dealmaking. portfolio company Birkenstock GmbH & Co.

It will come as no surprise that cross-border M&A is impacted by the world we live in, with geopolitical tensions, rising inflation and interest rates, currency fluctuations, and increased regulatory scrutiny all playing their part in making deals more challenging to execute.

Although 2022 saw a general decline in M&A activity in the life sciences industry compared to 2021’s frenetic pace (when deal volume was up 52% from 2020 ), life sciences deal flow in 2022 on balance remained strong despite the headwinds. Let’s dig in. Let’s dig in.

According to further figures from Dealroom , UK tech companies raised the most across Europe in 2022, securing $17.3bn in the first half of the year before the sector achieved combined market value of $1tn — meaning the UK had the most ground to lose.

Upgrade, a provider of personal credit lines and other consumer financial products, today announced that it’s agreed to acquire Uplift, the buy now, pay later (BNPL) vendor, for $100 million in cash and stock. Upgrade, however, thought a purchase made more sense — and it’s tough to argue with that logic.

It’s 2023, and the bonanza of M&A deals and IPOs we experienced during the pandemic has dried out. 2022 was a dismal year for IPOs, with a meager 181 US IPOs compared to 1035 in 2021 and 480 the year before. On the M&A side, global market turbulence has affected the number of mergers and […]

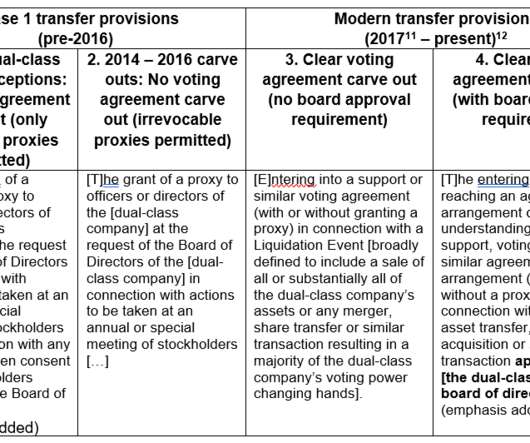

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders.

As cloud architecture continues to be more ubiquitous among organizations, increasingly what is more apparent is that many organizations are taking a hybrid approach, blending SaaS in private and public clouds with some products that remain on premises. Today, IBM made a big acquisition doubling down on the hybrid concept: it will pay $4.6

These characteristics, coupled with bakery manufacturers’ ability to continually innovate and adapt to consumer trends, have attracted investors and boosted M&A activity in recent years. bakery market has shown steady historical growth, with industry revenue rising roughly 4% annum from 2004 to 2022. The $75 billion U.S.

In a subdued year for global M&A, deal-making in the life sciences industry came in waves, with a busy fourth quarter generating cautious optimism heading into 2024. Big pharma dominated life sciences M&A, with more than two-thirds (69%) of M&A investment coming from big pharma, compared to just 38% in 2022.

M&A is a central part of SymphonyAI’s growth strategy as the company prepares for a potential private placement and, eventually, an IPO. “We’re Dhawan became CEO of SymphonyAI in 2022, replacing founder Romesh Wadhwani. The post On the Hunt: SymphonyAI’s M&A Algo appeared first on The Deal.

Even in 2022, when take-private deals hit a new record, they only accounted for 37% of the total value of transactions. Written by a top OfficeHours Coach; Original article published on October 16, 2023 In today’s world, there is much uncertainty around public markets.

The proposal arrives in the context of calls from various corners, including from SEC Chair Gary Gensler and former Acting Corp Fin Director John Coates, to treat SPACs as an alternative method of conducting an IPO under the SEC’s policy framework. See this PubCo post.)

Once improved, the exit can then take place, usually in the form of another sale or an Initial Public Offering (IPO), both of which are usually under the advice of an investment bank. Written by a Top OfficeHours Private Equity Coach Is PE a Good Fit for you? In investment banking, closing the transaction marks the end of the engagement.

Fundamentals of M&A: An Excerpt from The Art of M&A Book Series. By Alexandra Reed Lajoux, Board of M&A Standards/Founding Principal at CapEx . How Common are Postmerger Divestitures of Acquired Company Units? . It depends on how long a timeline for divestiture you are considering. What is a sell-off? . Recent U.S.

Following the completed merger, Redburn Atlantic will now operate as the equity capital markets execution arm of Rothschild & Co, with the aim of delivering participations for clients in IPOs, placements and block trades. By combining US and European research together in London, the new firm will benefit from a global industrial approach.

Bulge Bracket Bank Definition: The “bulge brackets” are the largest global banks that operate in all regions and offer all services – M&A, equity, debt, and others – to clients; they work on the biggest deals (usually $1 billion+) and have divisions for sales & trading , equity research , wealth management , corporate banking , and more.

This chart of PE deal activity from 2001 to 2022 in the Bain Capital Healthcare Private Equity report sums up the market quite well: In short, healthcare had never been a huge sector for private equity, but activity ramped up in the late 2010s into the early 2020s, and it’s now one of the top industries by dollar volume (right after tech).

As SPAC IPOs broke records – in both value and volume – in 2020 (and again in 2021), it was inevitable that stockholder litigation would follow. January 3, 2022), the Court of Chancery had the first opportunity, in connection with a motion to dismiss hearing, to consider application of Delaware law in the context of a deSPAC transaction.

Like US constitutional law, Delaware courts apply a tiered standard of judicial review to actions taken by the board of directors of corporations: Business judgment deference (rational basis). Enhanced scrutiny under Unocal and Revlon (intermediate scrutiny). The compelling justification standard articulated in Blasius (strict scrutiny).

General trends in tech M&A. Despite everyone’s efforts in 2021, including the rollout of vaccines and varying rounds of lockdowns and work-from-home mandates, a true “return to normal” for M&A dealmakers was foiled anew by COVID-19 and its variants. Tech M&A surged to a staggering $1.1 trillion(!)

2023’s much-discussed downturn in mergers & acquisitions – with global M&A volume and value down 6% and 17%, respectively, from 2022 – was largely driven by the slowdown in the tech sector, with global tech M&A volumes down 51% year over year, while other sectors saw marked increases. [1] billion leading the pack.

Tech M&A in 2022 was a tale of two halves. billion [1] during the first half of 2022 to $189.17 billion in the second half, resulting in total 2022 volume of $720.3 billion [1] during the first half of 2022 to $189.17 billion in the second half, resulting in total 2022 volume of $720.3 trillion. [2]

General trends in life sciences M&A. While 2020’s M&A landscape was characterized by whiplash volatility from choppy deal activity in the first half of the year to a surge in volume in the second half, that momentum accelerated in 2021, with no signs of slowing down heading into 2022. driven assets.

Unlike in 2023, when a Q4 dealmaking binge over the holidays led to the sector outperforming the market, life sciences M&A cut down and stuck with it throughout 2024. Unlike in 2023, when a Q4 dealmaking binge over the holidays led to the sector outperforming the market, life sciences M&A cut down and stuck with it throughout 2024.

This active M&A market continued for almost three years until mid-to-late 2022 when interest rates increased rapidly, making it much more expensive to buy or build new car wash locations. Beginning in 2020, there was a wave of announcements for private equity firms entering the car wash industry. Who will be the buyers?

After a rough 2023 , tech M&A in 2024 was slow to start but ended the year strong, with deal values up 32% from 2023 , well outpacing the overall M&A markets 10% growth in 2024. So is tech M&A back? Tech M&A may not be back, but its story is far from over. billion acquisition of Altair, IBMs pending $6.4

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content