[co-author: Ken Dai]

The real estate industry, one of the pillar sectors of the national economy, has played a pivotal role in China’s economic development since the reform and opening‑up. In recent years, driven by systemic factors such as economic restructuring, population decline, and slowing urbanization, the sector has undergone complex evolution. Any M&A transaction in the real estate industry—whether a merger, an equity or asset acquisition, or the formation of a new joint venture—that meets the statutory turnover thresholds must first be notified to the State Administration for Market Regulation (hereinafter “SAMR”) and approved before closing; if the parties have foreign turnover, filings may also be made with the relevant overseas antitrust authorities. This framework is known under the Anti‑Monopoly Law as the merger filing and review regime.

A statistical analysis of merger review cases from 2021 to July 2024 reveals that the real estate sector is characterized by a long industrial chain, numerous segmented markets, generally fragmented market structures, and pronounced regional competition among midstream and downstream property developers, operators, and property managers.1 Since 2022, there has been a significant drop in real estate M&A deals, with state-owned enterprises replacing private ones in market rescue efforts. Foreign M&A has been active, focusing on commercial real estate like offices in first and second-tier cities. Most deals involve horizontal or vertical business integration, with few pure investment‑style acquisitions. Transactions are mainly in residential, office buildings, and large‑scale retail real estate development, and property management services, with related markets becoming more concentrated.

-

Industrial Chain and Competitive Landscape of the Real Estate Sector

The “real estate industry” in this article encompasses all integrated economic activities involving land and buildings, including development, construction, operation, management, maintenance, decoration, and related services. Based on land‑use type, the industry is broadly divided into: residential real estate, commercial real estate, industrial and other real estate.

Real estate is among the leading sectors for M&A transactions in China. According to incomplete statistics, from 2021 to July 2024 there were 189 merger review cases in the real estate sector, representing 8% of all filings. A review of past cases shows that the industry’s value chain comprises multiple segments, chiefly: (1) upstream architectural design and construction, (2) midstream property development, operation, sales, and leasing—e.g., commodity and affordable housing in the residential segment; office buildings, retail of all scales, hotels, and long‑stay apartments in the commercial segment; industrial parks, etc., and (3) downstream services like property management. Furthermore, many real estate M&A transactions involve private‑equity investments targeting these segments.

Figure 1: Key Relevant Markets Involved in Real Estate Merger Filing Cases

In China’s upstream building design and construction segment, competition is diversified and follows a “central SOE–led + regional champion” pattern, with the overall market structure remaining highly fragmented. In the midstream development and operation segment, residential development has evolved into a dual-track competition between “national-brand developers” and “locally entrenched firms”, while commercial real estate is increasingly dominated by specialized operators such as CR Mixc Lifestyle and Longfor Paradise Walk. Logistics real estate, meanwhile, is controlled by capital-driven platforms like GLP and Vanke Logistics, resulting in a market landscape characterized by “one dominant player and several strong competitors.” In the downstream property management segment, low investment thresholds and modest startup capital requirements have led to a crowded market of small and medium-sized enterprises, resulting in extremely fierce competition.

In recent years, the overall development of the real estate industry has stalled, with private enterprises in many regions experiencing broken financing chains and struggling to maintain the ongoing housing construction projects. In response to this severe situation, several government departments have introduced a series of policy measures, such as restarting the equity financing mechanism for real estate enterprises. These measures aim to facilitate M&A and reorganization of related enterprises and ensure necessary financial support for their operations. Against this backdrop, leading enterprises are accelerating resource integration through acquisitions and mergers. However, regional small and medium - sized real estate companies still occupy niche markets, particularly in areas like urban renewal and affordable housing construction, where they maintain a competitive edge.

-

Characteristics and Trends in Real Estate Merger Review Cases

Based on the “Annual Report on China's Anti-Monopoly Law Enforcement” released by SAMR (hereinafter the “Annual Report”) and publicly disclosed simplified merger review cases, merger filings in China's real estate industry presents the following features:

-

Sharp Decline in Merger Filings Since 2022, with Sustained Low Levels in Recent Years

According to the Annual Report, SAMR concluded 72 merger filings in the real estate sector in 2021 and 43 in 2022. Moreover, SAMR’s publicly disclosed simplified merger review cases show that 47 such cases were closed in 2023 and 24 between January and July 2024.

These figures indicate that, owing to factors such as recurrent COVID-19 outbreaks, the emergence of debt-default risks among certain developers, and a slowdown in overall economic growth, the number of real estate merger filing has plunged since 2022 and has remained at a low level in recent years.

Figure 2: Number of Real Estate Merger Filing Cases (2021–2024)

-

State-Owned Enterprises Step In as Private Firms Retreat, with Foreign Investment Driving Commercial Real Estate M&A

According to publicly disclosed simplified merger review cases from 2021 through July 2024, since 2022 the number and proportion of filings in which private enterprises act as acquirers have plunged. By contrast, filings by state-owned enterprises have risen year by year, both in absolute terms and as a proportion of the total—from just 15% in 2021 to 53% in January–July 2024—clearly reflecting a trend of SOEs stepping in to stabilize the market.

Moreover, foreign investors have consistently shown strong enthusiasm for real estate. Since 2021, foreign-buyer filings have accounted for at least 25% of all cases, and reached 50% in both 2022 and 2023. Rather than targeting residential properties, these investors have focused predominantly on income-producing commercial assets such as office buildings. Geographically, their activity has been concentrated in first- and second-tier cities such as Beijing, Shanghai, Guangzhou, Shenzhen, and Chengdu, as well as surrounding hotspots.

Figure 3: Number of Merger Filing Cases in Real Estate (2021–2024) by Acquirer Nature

Figure 4: Proportion of Merger Filing Cases in Real Estate (2021–2024) by Acquirer Nature

Figure 5: Number and Proportion of Foreign Investment Merger Filing Cases in Real Estate Sub-sectors (2021–2024)

-

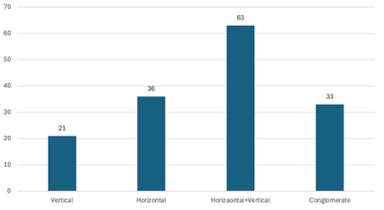

Strong Business Linkages among Parties, with Horizontal and Vertical M&A Dominating

Based on SAMR’s publicly disclosed simplified merger review cases from 2021 through July 2024, filings in the real estate sector show a high degree of business relatedness between the merging parties. Transactions aimed at horizontal or vertical integration account for 78% of all cases. Among these, cases involving both horizontal and vertical relationships between the parties represent 41%. Investment-oriented mixed acquisitions are relatively few, comprising only 22%.

Figure 6: Number of M&A Cases in Real Estate Merger Filing (2021–2024)

Figure 7: Proportion of M&A Cases in Real Estate Merger Filing (2021–2024)

-

Increasing Horizontal Concentration in Downstream Development, Operations, and Property Management

According to SAMR’s publicly disclosed simplified merger review cases from 2021 through July 2024, within the horizontal-integration category, transactions targeting downstream real estate development, operations, and property management occur far more frequently than those involving upstream construction and design. This indicates that downstream developers and property management companies are the primary acquisition targets in real estate M&A, and that market concentration in these downstream segments is steadily increasing.

Figure 8: Relevant Market Involvement in Horizontal Merger Filing Cases in Real Estate (2021–2024)

-

Outlook and Practical Tips for Enterpsies in the Real Estate Industry

The real estate industry, as a key pillar of China’s economy, has faced mounting challenges in recent years due to a variety of factors, and its M&A landscape has undergone significant shifts. Since 2022, transaction volumes have plunged. Under a fragmented market structure, state-owned enterprises’ market-rescue interventions and active foreign investment have become especially prominent; M&A deals have largely centered on business integration, and market concentration levels have been rising. In terms of market definition, mid- and downstream segments display distinctive characteristics—requiring segmentation by property nature and use—and exhibit pronounced city-level regional features.

Looking ahead, real estate firms must on one hand adapt to industry trends and seize the opportunities presented by state-owned enterprise participation and active foreign investment to optimize their business portfolios; on the other hand, when pursuing M&A transactions, they must rigorously uphold antitrust compliance—assessing in advance how their transaction may affect market competition, proactively submit filings and cooperating with reviews—so as to achieve transformation, upgrading, and sustainable development amid change, and to help the real estate industry revive during economic restructuring.

Note List

The statistical methodology is as follows: based on information from the merger filing publicity form for simplified procedure, transactions were screened, aggregated, and analyzed using keywords such as “housing”, “real estate”, “office building”, “residential” and “industrial park”. All data on merger filings in the real estate sector referenced in this article are derived from this methodology.